Table of Contents

Deregister for GST in Singapore is an important step for businesses that no longer meet the requirements for GST registration or have ceased taxable activities. Understanding when and how to deregister GST Singapore is essential to ensure full compliance with the Inland Revenue Authority of Singapore (IRAS) regulations.

Under IRAS rules, businesses may apply for GST deregistration if their taxable turnover falls below the threshold or if they stop making taxable supplies altogether. However, the process involves specific eligibility criteria, documentation, and post-deregistration obligations that must be carefully followed.

This guide explains when businesses should deregister for GST in Singapore, outlines the eligibility conditions, and walks through the key steps, requirements, and compliance responsibilities involved in the deregistration process.

Key Takeaways

- GST deregistration is required when your business no longer meets IRAS criteria (e.g., ceased operations, no taxable supplies, restructuring).

- You must apply within 30 days for compulsory cases; late action may lead to penalties.

- Continue GST obligations until IRAS approval, including charging GST and filing returns.

- Final compliance is critical: submit Form F8, account for assets (if applicable), and keep records for at least 5 years.

- Proper planning matters, voluntary deregistration can reduce costs but may impact input tax claims and future registration.

What it means to deregister for GST

GST deregistration refers to the formal cancellation of a business’s GST registration with IRAS. Once deregistered, the business will no longer charge GST on its sales or file GST returns. This marks a clear transition in the company’s tax obligations and reporting requirements.

There are two main types of deregistration: compulsory and voluntary. Compulsory deregistration applies when a business no longer meets the conditions for GST registration under IRAS rules. Voluntary deregistration, on the other hand, may be initiated by businesses that expect their taxable turnover to fall below the registration threshold or no longer see value in remaining GST-registered.

GST deregistration typically applies in situations such as cessation of business, restructuring, or reduced taxable turnover. For example, when a company stops operations, transfers its business, or changes its legal structure, it may no longer qualify for GST registration.

It is important to note that GST obligations continue until IRAS officially approves the deregistration. Businesses must continue charging GST, issuing tax invoices, and filing GST returns up to the effective date of cancellation. Stopping GST practices prematurely may result in non-compliance.

Therefore, obtaining IRAS approval is a critical step. Businesses should not assume that GST registration will be cancelled automatically or that obligations end once operations cease. Proper deregistration ensures compliance, avoids penalties, and supports a smooth transition to the next phase of business operations.

When you must deregister for GST (compulsory cases)

In Singapore, businesses are required to deregister for GST within 30 days if they no longer meet the criteria for GST registration. This is a compulsory obligation under IRAS regulations and applies in several key scenarios.

You must apply for GST deregistration if:

- Your business has ceased operations

When a company stops all business activities, it is no longer eligible to remain GST-registered.

- You no longer make taxable supplies

If your business no longer provides goods or services subject to GST, deregistration is required.

- Your business is transferred as a whole

If ownership is fully transferred to another party, the original entity must cancel its GST registration.

- There is a change in business structure

For example, transitioning from a sole proprietorship to a private limited company (Pte Ltd) creates a new legal entity. The original entity must GST deregister, and the new entity must assess its own GST registration requirements separately.

It is important to clarify that GST deregistration is not automatic, even if you have already closed your business with ACRA. Businesses must submit a separate application to IRAS to cancel their GST registration.

Additionally, when a new entity is formed during restructuring, it does not inherit the GST status of the previous business. Instead, it must independently evaluate whether it needs to register for GST based on its own turnover and activities.

Failure to deregister GST on time, within the required 30-day period, may lead to penalties imposed by IRAS. This often happens when businesses assume deregistration is automatic, overlook the deadline, or are preoccupied with other administrative tasks during closure or restructuring.

To remain compliant, businesses should proactively assess their GST status and ensure timely deregistration when required.

Voluntary deregistration eligibility

Businesses in Singapore may choose to deregister for GST voluntarily when they are no longer required to remain GST-registered under IRAS rules. This option is typically suitable for companies experiencing reduced activity or a sustained drop in revenue.

To qualify for voluntary deregistration, businesses must meet the following key conditions:

- Taxable turnover is below S$1 million in the past 12 months

- The business does not expect to exceed the S$1 million threshold in the next 12 months

- The forecast must be supported by objective evidence, such as financial statements, contracts, or business projections

It is important to note an additional requirement:

- If a business registered for GST voluntarily, it must remain registered for at least 2 years before applying for deregistration

This ensures that businesses do not frequently switch between registration and deregistration due to short-term fluctuations.

Before proceeding, businesses should carefully consider the implications. One key impact is the loss of input tax claims after deregistration. This means GST incurred on expenses, such as rent, software, or professional services, can no longer be recovered, potentially increasing operating costs.

Voluntary deregistration is often suitable for small businesses, freelancers, or companies downsizing operations, where the administrative burden of GST compliance outweighs the benefits. These benefits may include reduced filing requirements, lower compliance costs, and simplified financial management.

However, businesses should ensure that the drop in turnover is sustainable rather than temporary, as exceeding the threshold again would require re-registration and additional administrative effort.

Deregistration process and timeline

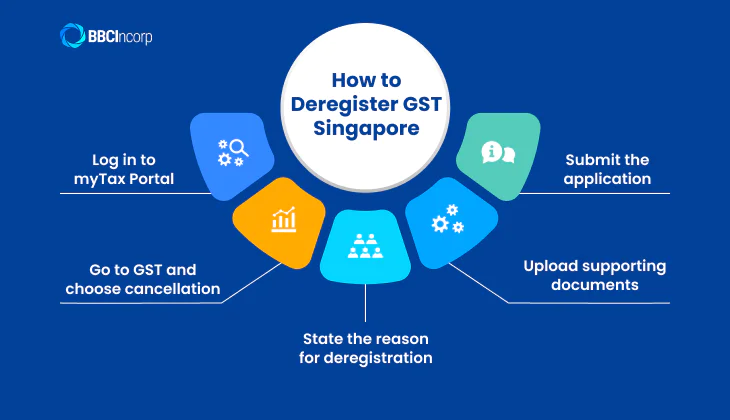

The process to deregister for GST in Singapore is relatively straightforward when handled correctly. Businesses must submit their application through the IRAS myTax Portal, which serves as the primary platform for GST-related matters.

Application process

To begin, businesses should:

- Log in to the myTax Portal.

- Navigate to “GST” and select “Apply for Cancellation of GST Registration”.

- Provide a clear reason for deregistration (e.g., business cessation or reduced turnover).

- Upload any supporting documents, such as financial statements or projections (for voluntary cases).

- Submit the application for review.

In some cases, alternative submission methods may be available, but the online portal remains the most efficient and recommended approach.

Processing timeline

- IRAS typically processes applications within the same day up to 10 working days, depending on the completeness and complexity of the submission.

- Businesses will receive an official notification confirming the approval and the effective cancellation date.

Important rules to follow

- Businesses must continue charging GST and filing returns until the official cancellation date.

- GST collection should only stop after IRAS approval is granted.

- Once deregistered, businesses must not issue tax invoices or charge GST on any sales.

Failing to follow these rules may result in compliance issues or penalties.

Effective date of deregistration

The effective date is determined and confirmed by IRAS in the approval notice. This date marks the official end of GST registration obligations.

Up to that point, businesses must fulfill all GST responsibilities, including filing their final GST return, settling any outstanding taxes, and maintaining proper records.

Final GST obligations after deregistration

Once GST deregistration is approved by IRAS, businesses must complete several final compliance obligations to formally close their GST responsibilities.

One of the key requirements is to file a final GST return (Form F8). This must be submitted within 1 month after the end of the final GST accounting period. The final return should accurately reflect all taxable activities up to the last day of GST registration.

Businesses must also account for GST on specific items, including:

- Business assets, such as inventory or fixed assets, if input tax was previously claimed and the total market value exceeds S$10,000.

- Supplies spanning the deregistration date, including transactions made before cancellation but invoiced or paid afterward.

It is important to ensure that all asset valuations are based on open market value at the point of deregistration, not original cost.

In addition, businesses must settle all outstanding GST payments promptly. Any payment delays may result in penalties or enforcement actions by IRAS.

Record keeping remains an ongoing obligation. Even after deregistration, businesses are required to maintain GST-related records for at least 5 years. This includes:

- Filed GST returns (including the final Form F8)

- Tax invoices and receipts

- Financial and transaction records

- Supporting documents for asset valuation

Maintaining complete and accurate records ensures readiness for potential audits and supports continued compliance even after GST obligations have officially ended.

Important considerations and common risks

While GST deregistration may seem straightforward, several common risks can lead to compliance issues if not properly managed.

One of the most frequent mistakes is missing the 30-day deadline for compulsory deregistration. Businesses that fail to apply on time may face penalties and unnecessary compliance exposure.

Another critical risk is stopping GST charges before receiving IRAS approval. GST must continue to be charged and reported until the official cancellation date. Premature changes can result in non-compliance and potential corrective actions.

Errors in the valuation of business assets are also common, especially when preparing the final GST return. Incorrect valuation, particularly not using open market value, may lead to underreporting or disputes with IRAS.

Businesses may also overlook final GST filing obligations, such as submitting the last GST return or accounting for outstanding transactions. Even if business activity has slowed or stopped, these requirements still apply.

Additionally, companies should be aware of the potential cash flow impact from final GST liabilities, including one-time GST payable on assets or unpaid taxes.

Best practices to ensure compliance:

- Review GST registration status regularly.

- Maintain accurate and up-to-date financial records.

- Plan deregistration timing carefully, especially around reporting periods.

- Seek professional support to ensure full compliance and avoid costly mistakes.

How BBCIncorp can help with GST deregistration

GST deregistration is not just about submitting a form. It also involves getting your tax treatment, final filings, and compliance steps right to avoid penalties and unnecessary tax exposure. BBCIncorp supports businesses in Singapore through its Accounting services in Singapore, helping you handle key tax and reporting obligations with greater accuracy and confidence.

Our team can help you assess your deregistration readiness, prepare the required supporting documents, handle your final GST-related filings properly, and guide you on the next compliance steps after deregistration. For businesses undergoing cessation, restructuring, or entity changes, our Company Secretary support can also help you stay on top of corporate records and statutory compliance requirements.

What we do for you:

- Quick eligibility check – Know immediately if you should deregister (and when)

- Hassle-free application – We prepare and submit everything correctly via myTax Portal

- Accurate final GST return – Including proper treatment of assets, stock, and outstanding GST

- Clear next steps – So you stay compliant even after deregistration

We’ve supported startups, SMEs, and international founders in Singapore, so we understand real-world scenarios, not just theory.

With BBCIncorp, you don’t have to second-guess IRAS rules. You get a reliable team that gets it done right the first time, so you can move on with your business confidently.

Conclusion

Deregister for GST is an essential step when your business circumstances change, and GST registration is no longer required. To remain compliant, businesses must meet IRAS eligibility conditions and follow the correct deregistration process, including submitting the application on time and continuing GST obligations until approval is granted.

Even after deregistration, responsibilities do not end immediately. Businesses are still required to complete final filings, settle outstanding GST, and maintain proper records for future reference or audits. Missing these steps can lead to penalties or unnecessary tax exposure.

Taking timely and well-informed action ensures a smooth transition out of GST registration. With the right support, businesses can avoid common pitfalls and stay fully compliant. BBCIncorp provides expert guidance to help you manage GST deregistration efficiently and with confidence in Singapore. Need support? Contact us at service@bbcincorp.com.

Frequently Asked Questions

How do I know if I need to deregister for GST in Singapore?

You should deregister if your business has ceased operations, no longer makes taxable supplies, or no longer meets IRAS GST registration requirements. If you’re unsure how do I deregister for GST, it’s important to first confirm whether your business still meets the criteria for GST registration.

Can I deregister for GST if my revenue is below S$1 million?

Yes, you may apply for voluntary deregistration if your taxable turnover is below S$1 million and not expected to exceed it in the next 12 months.

What is the fastest way to deregister GST in Singapore?

Apply online via the IRAS myTax Portal with complete and accurate information; processing typically takes the same day to 10 working days.

Do I need to file anything after IRAS approves GST deregistration?

Yes, you must file a final GST return (Form F8), settle any outstanding GST, and keep records for at least 5 years.

Can I stop charging GST once I apply to deregister for GST?

No, you must continue charging GST until IRAS officially approves your deregistration and confirms the effective date.

Do I need to deregister for GST if I change from a sole proprietorship to a private limited company?

Yes, the original entity must deregister, and the new company must assess its own GST registration separately.

What happens to input tax claims after I deregister GST?

You can no longer claim input tax on purchases after deregistration.

Can I deregister for GST if I still owe GST to IRAS?

Yes, but you must still declare and pay all outstanding GST in your final return.

Disclaimer: While BBCIncorp strives to make the information on this website as timely and accurate as possible, the information itself is for reference purposes only. You should not substitute the information provided in this article for competent legal advice. Feel free to contact BBCIncorp’s customer services for advice on your specific cases.

Industry News & Insights

Get helpful tips and info from our newsletter!

Stay in the know and be empowered with our strategic how-tos, resources, and guidelines.