Table of Contents

Zero-rated GST in Singapore offers a valuable advantage for businesses involved in cross-border transactions, allowing certain supplies to be taxed at 0% while still retaining input tax claims. However, applying the zero rate GST is not always straightforward. Misclassification between zero-rated and standard-rated supplies is a common issue and can lead to costly errors, penalties, or denied tax claims.

Understanding when GST can be charged at 0% versus the standard rate is essential for maintaining compliance and optimizing cash flow. This is particularly important for companies dealing with exports, international services, or complex supply chains.

This guide explains the scope of zero-rated GST, outlines the key conditions, and provides practical insights on applying it correctly in Singapore.

Key Takeaways

- Zero-rated GST applies only to specific cases: Mainly exported goods and international services. Not all overseas transactions qualify.

- 0% GST still allows input tax claims: You can recover GST on business expenses, improving cash flow and cost efficiency.

- Documentation is critical for compliance: Keep export proof, contracts, and payment records to support GST eligibility.

- Misclassification creates tax risk: Errors may lead to 9% GST exposure, penalties, and rejected claims.

- Align processes with IRAS rules: Regular reviews and early checks help ensure accurate GST treatment and smooth filing.

Scope of zero-rated GST in Singapore

In Singapore, zero-rated GST applies strictly to two categories of supplies: export of goods and qualifying international services. This limited scope is intentional, ensuring that the GST zero rated is used to support cross-border economic activity while maintaining a clear and controlled tax framework.

It is important to understand that zero-rated supplies are still considered taxable supplies, not exempt supplies. This distinction is critical. While businesses do not charge output GST (0%), they are still allowed to claim input tax on expenses incurred in making those supplies. This creates a tax-neutral position and protects business margins, particularly for export-driven operations.

Zero-rating is only available to GST-registered businesses. Companies that are not registered for GST cannot apply the 0% rate, nor can they recover input tax. As such, GST registration status directly impacts whether a business can benefit from zero-rating provisions.

From a broader perspective, zero-rated GST plays a strategic role in Singapore’s position as a global trade and services hub. By ensuring that exports are not burdened with domestic consumption tax, the system enhances international competitiveness and supports seamless cross-border transactions.

However, eligibility is not automatic. Businesses must ensure that each transaction falls clearly within the defined scope. Misclassification, such as incorrectly treating a local transaction as a zero rated supply, can lead to underpaid GST, penalties, and significant compliance risks.

In practice, businesses should approach zero-rating with a structured review process, confirming both the nature of the supply and the supporting documentation required under IRAS guidelines.

Zero-rated supplies: goods vs services

Export of goods

For goods to qualify as zero-rated, they must be physically exported out of Singapore. The key condition is not just the customer’s location, but the actual movement of goods beyond Singapore’s borders.

The supplier is responsible for ensuring that all export conditions are met. This includes maintaining proper documentation such as commercial invoices, customs permits, shipping documents, and airway bills. Without sufficient proof, the transaction may be reclassified as a standard-rated supply.

A key distinction exists between direct and indirect exports. In direct exports, the supplier manages the shipping process and retains control over documentation, making it easier to apply zero-rating. In indirect exports, where the buyer arranges shipment, zero-rating is generally not allowed unless the supplier can still obtain valid proof of export.

Timing also matters. Goods must typically be exported within a prescribed period (commonly within 60 days from the earlier of invoice date or payment receipt). Failure to meet this requirement can invalidate the zero-rated treatment.

International services

Zero-rating for services is more nuanced. Not all services provided to overseas clients qualify. To be zero-rated, services must fall under Section 21(3) of the GST Act, which defines qualifying international services.

Eligibility depends on both the nature of the service and the location of the customer. Generally, services must be supplied to a person belonging outside Singapore or performed entirely outside the country.

Common examples include:

- International transport and freight services.

- Cross-border consulting or advisory services.

- Digital services (e.g., marketing, IT, or software support) are provided to overseas clients.

However, simply invoicing a foreign client does not guarantee zero-rating. If the service is consumed in Singapore or linked to local business activities, it may still be subject to standard GST.

Given the complexity, businesses should carefully assess each transaction and maintain clear documentation to support the correct GST treatment.

Conditions and documentation requirements

Applying zero rated GST Singapore requires more than just identifying a qualifying transaction. Businesses must meet strict legal conditions and maintain proper documentation to support the 0% GST treatment.

Legal requirement to qualify for zero-rating

Zero-rating is only allowed when all conditions under GST regulations are fully satisfied. The responsibility lies with the business to prove eligibility. If there is any uncertainty or missing evidence, the transaction should not be treated as zero-rated.

Export evidence for goods

For exported goods, businesses must show that the goods have physically left Singapore. Key supporting documents include:

- Shipping documents (e.g. bill of lading, airway bill).

- Customs export permits.

- Commercial invoices.

These documents must be consistent and complete. Any discrepancies may result in the supply being reclassified.

Documentation for international services

For services, the focus is on proving both the nature of the service and the location of the client. Businesses should retain:

- Contracts or service agreements.

- Invoices and proof of payment.

- Supporting communication (e.g., emails, project scope).

These documents help demonstrate that the service qualifies under GST rules.

Determining customer belonging status

A critical step is identifying where the customer “belongs” for GST purposes. This is not just the billing address; it includes where the business is legally established or operates. Misjudging this can lead to incorrect GST treatment.

Consequence of non-compliance

If any condition is not met, the default treatment applies: standard-rated GST (9%). Businesses may need to account for GST retrospectively, along with potential penalties and interest.

Best practice: Maintain clear, consistent, and well-organised records. Strong documentation is essential to support zero-rating and avoid compliance risks.

Key distinction: zero-rated vs exempt supplies

At a glance, both zero-rated and exempt supplies involve no GST charged to customers. However, the difference lies in how input tax is treated, and this has a direct impact on business costs and tax efficiency.

Zero-rated supplies

- GST rate: 0%

- Input tax claim: Allowed.

- Eligibility: Only for GST-registered businesses.

Zero-rated supplies are still classified as taxable supplies, even though no GST is charged. This means businesses can recover input tax on related expenses such as materials, logistics, or professional services.

This treatment is especially beneficial for export-oriented businesses, as it preserves margins and supports cash flow while remaining fully compliant.

Exempt supplies

- GST rate: No GST charged.

- Input tax claim: Not allowed.

Exempt supplies are not subject to GST, but businesses cannot claim input tax on expenses related to these activities. This effectively increases the cost base, as GST incurred becomes a non-recoverable expense.

Common examples of exempt supplies in Singapore include:

- Financial services (e.g., loans, insurance).

- Sale or lease of residential property.

Practical impact

The distinction directly affects cost structure and tax recovery. Businesses making zero-rated supplies benefit from input tax refunds, while those dealing with exempt supplies may face higher operational costs due to unrecoverable GST.

Misunderstanding this difference can lead to incorrect GST treatment, disallowed claims, and compliance issues.

Compliance risks and practical considerations

Applying zero-rated GST incorrectly is one of the most common compliance risks for businesses in Singapore. While the 0% rate is attractive, it requires strict adherence to IRAS rules.

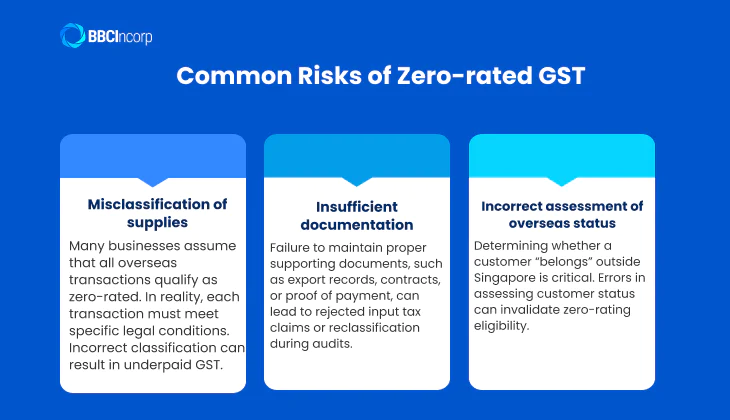

Common risks

- Misclassification of supplies

Many businesses assume that all overseas transactions qualify as zero-rated. In reality, each transaction must meet specific legal conditions. Incorrect classification can result in underpaid GST.

- Insufficient documentation

Failure to maintain proper supporting documents, such as export records, contracts, or proof of payment, can lead to rejected input tax claims or reclassification during audits.

- Incorrect assessment of overseas status

Determining whether a customer “belongs” outside Singapore is critical. Errors in assessing customer status can invalidate zero-rating eligibility.

Consequences

If zero-rating conditions are not met, IRAS may reclassify the supply as standard-rated, requiring businesses to account for 9% GST retrospectively. This may also include penalties and interest, especially if errors persist over multiple reporting periods.

Beyond financial impact, non-compliance can disrupt operations, trigger audits, and affect business credibility.

Practical considerations

To manage these risks, businesses should:

- Conduct regular internal reviews of GST treatment

- Ensure consistent application of IRAS guidelines

- Maintain accurate and complete documentation

Engaging professional support can further reduce risk. Experienced advisors help validate classifications, review documentation, and ensure that GST reporting aligns with regulatory expectations, providing both compliance assurance and operational confidence.

How to claim input tax on zero-rated supplies

Claiming input tax is one of the key benefits of making zero-rated supplies. Even though you charge 0% GST on sales, you can still recover the GST paid on business expenses, helping reduce costs and improve cash flow.

What you need to claim input tax on a zero-rated supply

To claim input tax correctly, your business must meet these core conditions:

- Be GST-registered in Singapore.

- Ensure the expense is used for business purposes and directly linked to zero-rated supplies.

- Hold valid tax invoices issued by GST-registered suppliers.

- Confirm that the transaction qualifies as zero-rated under IRAS rules (e.g., export of goods within the required timeline or qualifying international services).

- File GST returns (F5) accurately and on time via IRAS myTax Portal.

If your input tax exceeds output tax, you may claim a GST refund for the difference. However, IRAS will review whether the claim is valid and properly supported.

Keep the right documents for zero-rated GST claims

Documentation is critical. Without proper records, input tax claims may be rejected during audits. You should maintain:

- Supplier invoices and receipts.

- Export documents (e.g., shipping records, customs permits).

- Contracts or service agreements for overseas services.

- Proof of payment (bank transfers, transaction records).

All documents should be accurate, consistent, and clearly linked to the zero-rated supply. Strong record-keeping not only supports your claims but also ensures smoother GST filing and faster refund processing.

How BBCIncorp helps with zero-rated GST compliance

Zero-rated GST can bring valuable tax benefits, but only when it is applied accurately and supported by the right documentation. At BBCIncorp, we help businesses manage this area with a structured and practical compliance approach, backed by our accounting services in Singapore.

Our team ensures your zero-rated transactions are accurately classified, aligned with IRAS rules, and supported by proper documentation. From day one, we help you review whether your supplies qualify, reducing the risk of misclassification and costly rework later.

Beyond classification, BBCIncorp handles the full accounting and tax compliance process. This includes bookkeeping, GST filing, and preparation of statutory financial statements, ensuring that all figures reported are consistent, complete, and audit-ready.

We also support businesses in:

- Preparing and reviewing GST returns (F5).

- Validating input tax claims and supporting documents.

- Aligning financial data with regulatory requirements.

- Managing related compliance, such as annual tax filing and XBRL preparation.

Our workflow is designed to be seamless. From initial consultation to filing with authorities and ongoing support after submission, we ensure your business remains compliant without disrupting daily operations.

With BBCIncorp, you gain more than just execution; you gain clarity, control, and confidence in your GST position, especially when dealing with cross-border transactions and zero-rated supplies.

Conclusion

Zero-rated GST in Singapore offers clear advantages for cross-border businesses, but only when applied correctly. It is limited to specific qualifying supplies, and accurate classification is essential to ensure compliance with IRAS requirements. More importantly, proper documentation is what ultimately determines whether your transactions are eligible for 0% GST treatment. Without it, businesses risk reclassification, unexpected tax exposure, and penalties.

Given the technical nature of zero-rated rules, taking a structured and informed approach is key. From assessing eligibility to maintaining audit-ready records, each step plays a role in safeguarding your tax position. BBCIncorp supports businesses in navigating GST complexities with confidence, ensuring compliance while optimising tax outcomes. For expert guidance tailored to your business, reach out to us at service@bbcincorp.com.

Frequently Asked Questions

How do I know if my supply qualifies as zero-rated GST?

Your supply must fall under export of goods or qualifying international services (per Section 21 of the GST Act) and meet all IRAS conditions, including proper documentation.

Can I claim input tax on a zero-rated supply?

Yes. Zero-rated supplies are taxable at 0%, so you can still claim input tax on related business expenses.

Is residential property rental a zero-rated supply?

No. It is an exempt supply, meaning no GST is charged, and input tax cannot be claimed.

What happens if I file my GST return late?

Late filing may result in penalties, possible enforcement actions, and delays in GST refunds.

What is the current GST rate in Singapore?

The standard GST rate in Singapore is 9% (as of 2026). If you’re exploring what is zero rated GST, note that certain qualifying supplies are taxed at 0% instead of the standard rate.

Disclaimer: While BBCIncorp strives to make the information on this website as timely and accurate as possible, the information itself is for reference purposes only. You should not substitute the information provided in this article for competent legal advice. Feel free to contact BBCIncorp’s customer services for advice on your specific cases.

Industry News & Insights

Get helpful tips and info from our newsletter!

Stay in the know and be empowered with our strategic how-tos, resources, and guidelines.