Table of Contents

Hong Kong remains one of Asia’s leading international financial centres and a popular jurisdiction for company formation. Once a company is incorporated, opening a business bank account is an essential next step for receiving payments, managing business expenses, and supporting day-to-day operations.

Besides long-established banks, founders can now choose from licensed virtual banks and fintech platforms that offer different onboarding processes, pricing models, and digital capabilities.

This guide compares the five best business bank accounts in Hong Kong for startups in 2026. Whether you’re a local entrepreneur or an overseas founder, this comparison will help you identify the most suitable banking solution for your startup.

Key Takeaways

- Hong Kong businesses can choose from traditional banks, virtual banks, and fintech platforms, each offering different advantages depending on their banking needs.

- HSBC and Hang Seng Bank are well-suited for businesses seeking comprehensive banking services, while Airwallex, ZA Bank, and Statrys offer faster, digital-first alternatives.

- Traditional banks generally have stricter KYC requirements and longer approval times, whereas digital providers often provide quicker onboarding for eligible businesses.

- When comparing the best business bank accounts in Hong Kong, evaluate account opening requirements, fees, international payment capabilities, and digital tools, not just the initial cost.

- Costs vary widely: traditional banks may charge opening fees, monthly fees, or require minimum balances, while many digital providers offer low-cost or fee-free options.

How we evaluated the best business bank accounts in Hong Kong

Choosing a business bank account involves more than comparing fees or brand reputation. To compile this list, we reviewed publicly available information from each provider’s official website and assessed the factors most relevant to startups, SMEs, and international founders opening a business account in Hong Kong.

Our evaluation considered the following criteria:

- Account eligibility: Whether the provider accepts startups, overseas founders, and newly incorporated companies, as well as the documentation and KYC requirements.

- Account opening process: The ease of application, availability of remote onboarding, expected approval timeline, and overall customer experience.

- Fees and pricing: Account opening fees, monthly maintenance charges, minimum balance requirements, transfer fees, and foreign exchange costs.

- Banking features: Multi-currency support, international payment capabilities, business debit or corporate cards, expense management, and additional financial services.

- Digital banking experience: Online banking functionality, mobile app quality, software integrations, and day-to-day account management.

- Overall value for startups: How well each provider balances accessibility, features, pricing, scalability, and long-term support for growing businesses.

Quick comparison of the best business bank accounts in Hong Kong

| Provider | Best for | Monthly fee | Multi-Currency support | Minimum deposit |

| HSBC (Hong Kong) | Comprehensive banking services | Varies; HKD 1,300 for online applications and HKD 1,600 for all other application methods. | Yes | Varies |

| Airwallex | Global payments and multi-currency management | HKD 499 /month to HKD 2,499+ | Yes | No minimum deposit |

| Hang Seng Bank | Local banking ecosystem | Varies | Limited | Varies |

| ZA Bank | Digital-first banking | No monthly fee | Limited | No minimum deposit |

| Statrys | Flexible banking for non-residents | Zero monthly fees | Yes | No minimum deposit |

Disclaimer: Data verified as of July, 2026. Pricing and service offerings may change over time. Please check the official websites of the respective providers for the most accurate and up-to-date information regarding their prices and services.

The 5 best business bank accounts in Hong Kong for startups

The best business bank accounts in Hong Kong for startups include Airwallex, HSBC, Statrys, Aspire, and ZA Bank. The right choice depends on your startup’s business model, banking needs, and whether you require traditional branch services or a digital-first solution.

HSBC – The most comprehensive banking solution for growing businesses

As Hong Kong’s largest bank, HSBC has been serving businesses since 1865 and remains one of the most established banking partners in the market.

Its broad portfolio of financial services, combined with a presence across 62 countries and territories, makes it a strong choice for startups and SMEs that expect to expand beyond Hong Kong or require more sophisticated banking as they grow.

Businesses can access multi-currency accounts, payment and collection services, foreign exchange, trade finance, business lending, and cash management through a single banking relationship.

HSBC also offers online and mobile banking alongside an extensive branch network, allowing companies to manage both everyday transactions and more complex financial needs from one platform.

Pros:

- Broad portfolio of business banking products and services

- Strong support for cross-border payments and foreign exchange

- Access to financing, trade finance, and cash management solutions

- Reliable online and mobile banking backed by a large branch network

- Established reputation with extensive experience serving international businesses

Cons:

- Account opening may take longer due to comprehensive compliance reviews

- Documentation requirements can be more extensive, particularly for overseas founders

- Account maintenance fees may apply depending on the account package and eligibility

- May offer more features than very early-stage startups require

Best for: HSBC is suitable for all types of business, seeking for a long-term banking partner, especially those expecting higher transaction volumes, cross-border business activities, or future financing needs.

Airwallex – A powerful multi-currency account for global businesses

Unlike a traditional bank, Airwallex combines business accounts, payments, foreign exchange, cards, and expense management into a single platform.

This technology-first approach makes it a popular choice for startups, e-commerce businesses, SaaS companies, and SMEs looking to scale internationally without relying on multiple financial providers.

Eligible Hong Kong businesses can use Airwallex to receive customer payments, pay overseas suppliers, manage business expenses, and automate financial workflows through integrations with leading accounting and e-commerce platforms.

Its streamlined onboarding process and intuitive online platform also make it an attractive alternative to traditional business banking for companies prioritizing speed and operational efficiency.

Pros:

- Fast local transfers across 120+ countries and regions

- SWIFT transfers to more than 200 countries and territories account

- Multi-currency account designed for global business operations

- Competitive foreign exchange rates for international payments

- Corporate cards with integrated expense management

- Fast, fully digital onboarding and account management

- Integrates with leading accounting, ERP, and e-commerce platforms

Cons:

- Not a full-service traditional bank

- Does not provide conventional business lending or trade finance

- Limited cash deposit and branch banking services

- Certain products, features, and eligibility requirements vary by jurisdiction

Best for: Airwallex is best suited for startups, e-commerce businesses, SaaS companies, and internationally focused SMEs that frequently send or receive payments across multiple markets.

Through the BBCIncorp x Airwallex partnership, eligible Hong Kong businesses can streamline both company incorporation and business banking setup.

Hang Seng Bank – A trusted option for companies serving the local market

Founded in 1933, Hang Seng Bank is widely recognised as Hong Kong’s leading local bank and serves nearly 4 million customers. As a member of the HSBC Group, it combines deep local market expertise with the backing of one of the world’s largest banking groups.

For startups and SMEs operating primarily in Hong Kong, Hang Seng offers a comprehensive range of business banking services supported by an extensive branch network and well-developed digital banking capabilities.

Businesses can access everyday banking, payment and collection services, multi-currency accounts, foreign exchange, trade finance, business financing, and cash management through a single banking relationship.

The bank also continues to invest in digital innovation, offering online and mobile banking, remote account opening for eligible businesses, and integrated payment solutions that help companies manage day-to-day operations more efficiently.

Pros:

- Strong reputation as one of Hong Kong’s leading domestic banks

- Comprehensive banking solutions for local SMEs and growing businesses

- Extensive branch network with robust online and mobile banking

- Access to business financing, trade finance, and cash management services

- Member of the HSBC Group, providing additional financial strength and expertise

- Consistently recognised for SME banking and digital banking innovation

Cons:

- Account opening may involve detailed compliance checks and documentation

- International banking capabilities are not as extensive as HSBC’s global network

- Account maintenance fees may apply depending on the account package

- May be less suitable for businesses with significant overseas operations

Best for: Hang Seng Bank is best suited for startups and SMEs whose primary operations are based in Hong Kong. It is an excellent choice for businesses looking for a well-established local banking partner with comprehensive business banking services, strong digital capabilities, and convenient access to branch support.

ZA Bank – A digital-first choice for startups

ZA Bank is designed for businesses and entrepreneurs who prefer a fully online banking experience. Without relying on physical branches, the bank delivers account opening, payments, transfers, and day-to-day banking through a single mobile app and online platform.

Its streamlined onboarding process and intuitive interface make it particularly appealing to startups and small businesses seeking a fast and convenient way to manage their finances.

Beyond everyday banking, ZA Bank supports multi-currency accounts, global transfers, digital payment services, and business spending through an integrated platform.

Businesses can also benefit from 24/7 banking access and a range of digital financial services, making ZA Bank a practical option for companies that prioritise efficiency and mobile-first banking.

Pros:

- Fully digital account opening and banking experience

- Business account application completed entirely online

- 24/7 access through web and mobile banking

- Multi-currency account supporting major global currencies

- International transfers through SWIFT and other payment channels

- Modern, user-friendly digital banking platform

- No minimum deposit requirement for account opening

Cons:

- No physical branch network for in-person banking support

- Fewer corporate banking services than traditional banks

- Limited access to business lending and trade finance solutions

- Better suited for everyday banking than complex corporate banking needs

Best for: ZA Bank is best suited for startups, freelancers, and small businesses looking for a fast, digital-first banking experience. It is an excellent option for companies that primarily manage their finances online and require straightforward business banking rather than a full suite of corporate financial services.

Statrys – A flexible alternative for international founders

Statrys is a Hong Kong-based fintech platform that combines business accounts with company incorporation, accounting, and payment services.

Rather than functioning as a traditional bank, Statrys focuses on reducing administrative work by bringing essential back-office tools together in one platform. This makes it an attractive option for founders managing cross-border businesses or operating remotely.

Additionally, Statrys offers international payments, competitive foreign exchange services, company incorporation support, and accounting solutions.

Unlike many digital financial platforms, it also places a strong emphasis on human support, providing businesses with a dedicated customer service team instead of relying primarily on automated chatbots.

This combination of financial services and personalized support has helped Statrys become a popular choice among SMEs expanding across Asia.

Pros:

- Multi-currency business account with competitive FX rates

- Business payments and foreign exchange on a single platform

- Company incorporation and accounting services are available alongside banking services

- Dedicated customer support from real account specialists

- Transparent pricing with a straightforward digital platform

- Well-suited for businesses operating remotely or across multiple markets

Cons:

- Does not provide the full range of commercial banking products, such as business loans

- Smaller service ecosystem than large international banking groups

- Physical banking services and branch access are limited

Best for: Statrys is best suited for international founders, remote businesses, consultants, and SMEs that need a flexible multi-currency account alongside company incorporation, payment, and accounting services.

Overview of business banking in Hong Kong

Businesses in Hong Kong generally have three types of providers to choose from, each offering distinct advantages depending on their banking needs.

| Provider type | Key advantages | Considerations |

| Traditional banks | Comprehensive banking services, lending, trade finance, cash management, and branch support | Longer onboarding, stricter compliance reviews, and more documentation requirements |

| Virtual banks | Fully online account opening, intuitive mobile banking, and streamlined day-to-day banking | More limited product offerings, particularly for lending and trade finance |

| Fintech platforms | Multi-currency accounts, competitive FX rates, cross-border payments, and business software integrations | May not offer the full range of regulated banking products available from traditional banks |

Opening a corporate bank account in Hong Kong has become more demanding as banks strengthen Know Your Customer (KYC) and Anti-Money Laundering (AML) checks.

Businesses are often required to provide detailed information about their ownership, operations, source of funds, and expected transactions, which can lead to longer approval times.

At the same time, startups and foreign founders have more banking options than ever. Alongside traditional banks, virtual banks and fintech platforms offer faster onboarding, digital-first services, and efficient cross-border payments, allowing businesses to choose a solution that best fits their operational needs.

What should startups look for in a business bank account?

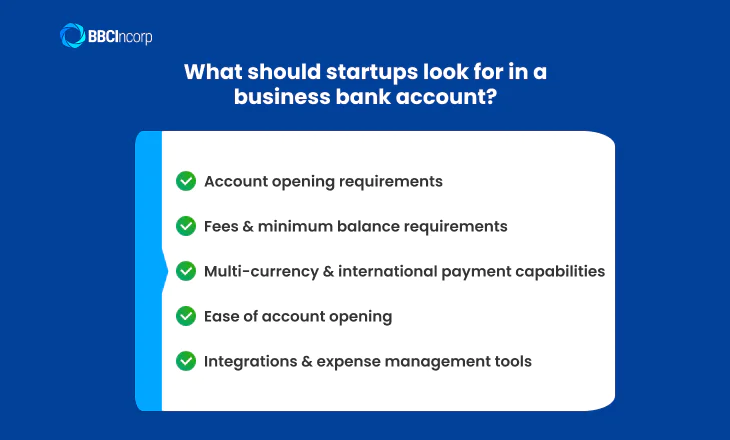

The right business bank account should support both your current operations and future growth. Beyond basic banking services, startups should evaluate factors such as account eligibility, costs, international payment capabilities, and digital tools to ensure the account aligns with their business model.

- Account opening requirements: Eligibility and documentation requirements vary significantly between providers. Traditional banks often require more extensive due diligence, while virtual banks and fintech platforms typically offer a simpler application process. Before applying, check whether the provider accepts overseas founders, newly incorporated companies, or businesses operating in your industry.

- Fees and minimum balance requirements: Compare the total cost of maintaining the account, including monthly maintenance fees, transfer charges, foreign exchange fees, and minimum balance requirements. Some digital providers offer low-cost or no-monthly-fee accounts, which can help startups reduce operating expenses during the early stages.

- Multi-currency and international payment capabilities: For businesses serving overseas customers or suppliers, efficient cross-border banking is essential. Look for providers that support multi-currency accounts, competitive foreign exchange rates, and low-cost international transfers to simplify global transactions.

- Ease of account opening: The application process can vary from a few minutes to several weeks, depending on the provider’s compliance procedures. If speed is a priority, consider providers that offer fully digital onboarding, remote identity verification, and online document submission.

- Integrations and expense management tools: Many modern banking platforms integrate with accounting software, payment gateways, and expense management tools. These integrations can automate bookkeeping, simplify reconciliation, and improve financial visibility, helping startups spend less time on administrative tasks.

How much does it cost to open a business account in Hong Kong?

The cost of opening a business account in Hong Kong varies depending on the provider you choose. Traditional banks generally charge account opening or administration fees and may require a minimum balance, while many virtual banks and fintech platforms have lower upfront costs or no monthly maintenance fees.

| Cost component | Typical range | Notes |

| Account opening fee | HK$0–HK$10,000+ | Many fintech providers charge no opening fee, while traditional banks may charge more for overseas or complex company structures. |

| Initial deposit | HK$0–HK$10,000+ | Some providers require an initial funding amount, while others do not. |

| Monthly maintenance fee | HK$0–HK$500 | Often waived if the required average balance is maintained. |

| Minimum balance requirement | HK$0–HK$50,000+ | Requirements vary significantly by bank and account package. |

| International transfer fees | Varies by provider | In addition to transfer fees, foreign exchange margins may apply. |

Conclusion

Choosing the best business bank account in Hong Kong depends on your company’s size, business model, and growth plans.

Traditional banks are well-suited for businesses seeking comprehensive financial services and long-term banking relationships, while virtual banks and fintech platforms offer faster onboarding and flexible digital solutions for startups and international founders.

By comparing account requirements, fees, payment capabilities, and digital features, you can find a banking solution that supports both your day-to-day operations and future expansion. Selecting the right provider from the start can help streamline financial management and position your business for long-term success.

Frequently Asked Questions

Which bank is best for business accounts in Hong Kong?

There is no single best option for every startup. Traditional banks such as HSBC and Hang Seng Bank are ideal for businesses seeking comprehensive banking services and long-term financing, while digital providers like ZA Bank and fintech platforms such as Airwallex and Statrys are better suited for startups prioritising fast onboarding, multi-currency capabilities, and international payments.

Can foreigners open a business bank account in Hong Kong remotely?

Yes, some providers allow eligible overseas founders to complete the application remotely. Many virtual banks and fintech platforms offer fully online onboarding, while traditional banks may require additional documentation or, in some cases, request an in-person meeting depending on the company’s profile, ownership structure, and compliance assessment.

What documents do I need to open a Hong Kong business bank account?

Requirements vary by provider, but businesses are typically asked to provide the company’s Certificate of Incorporation, Business Registration Certificate, constitutional documents, identification and proof of address for directors and beneficial owners, and information about the company’s business activities.

Some providers may also request contracts, invoices, or other documents to verify the source of funds and expected transactions.

How long does it take to open a business bank account in Hong Kong?

The timeline depends on the provider and the complexity of the application. Digital banks and fintech platforms may approve straightforward applications within a few business days, while traditional banks often require one to several weeks to complete compliance checks.

Applications involving overseas shareholders or more complex ownership structures may take longer.

Can I get professional support with opening a Hong Kong business bank account?

Yes. Many corporate service providers, like BBCIncorp, offer business account opening support alongside company incorporation services.

They can help prepare the required documents, review your application, communicate with the bank or fintech provider, and recommend the most suitable banking solution based on your company’s structure and business activities.

Disclaimer: While BBCIncorp strives to make the information on this website as timely and accurate as possible, the information itself is for reference purposes only. You should not substitute the information provided in this article for competent legal advice. Feel free to contact BBCIncorp’s customer services for advice on your specific cases.

Industry News & Insights

Get helpful tips and info from our newsletter!

Stay in the know and be empowered with our strategic how-tos, resources, and guidelines.