Table of Contents

Hong Kong is widely regarded for its simple, low, and business-friendly tax regime, making it an attractive hub for foreign investors and international companies. Hong Kong corporate tax rate, which is transparent, competitive, and designed to support sustainable business growth. This favourable structure has played a key role in drawing regional headquarters, trading companies, and global startups to Hong Kong.

For the 2024/25 tax year, digital filing is more common, and compliance standards are higher. Doing so, companies should understand how the Hong Kong corporate tax rate applies before incorporation or tax planning. This helps reduce risks and improve tax efficiency.

Key takeaway:

- Hong Kong offers a two-tiered corporate tax rate, 8.25% on the first HKD 2M and 16.5% above, under a territorial tax regime.

- Allowable deductions, industry incentives, and Hong Kong corporate tax exemption for offshore profits.

- Accurate profit calculation, timely corporate income tax filing in Hong Kong, and proper documentation.

Overview of corporate income tax in Hong Kong

Understanding corporate income tax in Hong Kong is essential for companies planning to establish operations, manage cross-border income, or optimize tax exposure. Rather than applying complex global tax rules, Hong Kong adopts a straightforward framework that focuses on the source of profits and limits unnecessary compliance burdens.

Territorial source principle and tax scope

A core concept of Hong Kong corporate tax is the territorial source principle. Under this principle, profits are taxable only when they arise in or are derived from Hong Kong. Income generated entirely outside Hong Kong may qualify for a Hong Kong corporate tax exemption, provided the company can demonstrate that the profits are offshore in nature.

In practice, profit sourcing is determined based on the actual activities that generate the income. Factors such as where core operations are conducted, where contracts are negotiated and executed, and where key management decisions take place are carefully reviewed. For trading businesses, the locations of purchase and sale activities are particularly important.

These principles form the foundation of Hong Kong profits tax, which governs how business income is assessed and taxed under Hong Kong law.

Entities subject to Hong Kong profits tax

Hong Kong profits tax applies to entities carrying on a trade, profession, or business in Hong Kong. This includes corporations, partnerships, and trustees. Individuals who earn income from business or self-employment activities are also subject to profits tax.

By contrast, individuals earning income from employment are taxed under salaries tax, which follows a separate assessment mechanism. Correctly classifying income types is essential to ensure proper tax treatment and avoid compliance risks.

Key features of Hong Kong’s tax system

One of the strongest advantages of the Hong Kong tax system is its simplicity. Hong Kong does not impose VAT, GST, capital gains tax, or withholding tax on dividends, interest, or royalties, subject to certain conditions. Combined with minimal reporting requirements, this structure significantly reduces administrative burden and supports efficient business operations.

Hong Kong corporate tax rate and tax bands explained

Rates are applied only after allowable deductions, expenses, and tax adjustments have been properly accounted for. This approach helps companies calculate liabilities accurately while maintaining transparency.

Standard Hong Kong corporate tax rate

The current standard Hong Kong corporate income tax rate for corporations is 16.5% of assessable profits. This rate applies to profits that are taxable under the territorial source principle. When compared with many global and regional markets, Hong Kong remains highly competitive.

Corporate tax rates in other major economies often exceed 20%, while some Asian jurisdictions impose additional indirect taxes or complex surcharges.

Importantly, the 16.5% rate applies only after deductible expenses, capital allowances, and approved tax reliefs are taken into account. As a result, the effective tax burden for many companies may be lower than the headline rate, especially for businesses with operational substance and proper documentation.

Two-tiered Hong Kong corporate income tax rate system

Hong Kong operates a two-tiered profits tax system to support small and medium-sized enterprises. Under this regime, corporations are taxed at 8.25% on the first HKD 2 million of assessable profits. Any remaining profits above this threshold are taxed at the standard rate of 16.5%.

Tax rates for unincorporated businesses

Unincorporated businesses, such as sole proprietorships and partnerships, are subject to different rates. Under the two-tier system, the first HKD 2 million of assessable profits is taxed at 7.5%, while profits above this amount are taxed at the standard rate of 15%.

For example, a sole proprietor providing consulting services or a small partnership operating a trading business would fall under this structure. Although the rates are slightly lower than those for corporations, unincorporated businesses should also consider legal liability, scalability, and compliance obligations when choosing a business form.

Allowable deductions, incentives, and corporate tax exemptions

Hong Kong allows businesses to deduct expenses that are wholly, exclusively, and necessarily incurred in the production of assessable profits. When combined with targeted tax incentives and exemption regimes, these rules provide legitimate ways for companies to reduce their taxable income while remaining fully compliant.

Common deductible business expenses

In general, businesses may deduct routine operating costs such as rental expenses for business premises, employee-related costs including salaries and mandatory contributions, utilities, professional and consultancy fees, marketing and advertising expenses, and irrecoverable bad debts arising from normal business activities.

Additionally, Hong Kong provides capital allowances on qualifying assets, such as machinery, equipment, and office systems. These allowances function as tax depreciation and help spread the cost of capital assets over time, further reducing assessable profits.

Key corporate tax incentives and industry-specific schemes

Beyond standard deductions, Hong Kong offers targeted incentives to support innovation and specialised sectors. Companies engaged in qualifying research and development activities may benefit from R&D super deductions.

Multinational groups may also take advantage of the corporate treasury centre regime, which offers a preferential tax rate for eligible treasury activities carried out in Hong Kong.

Specific industries are supported through dedicated regimes, including tax concessions for aircraft leasing businesses and preferential treatment for captive insurance companies. Each incentive comes with clear eligibility criteria, substance requirements, and compliance obligations.

Hong Kong corporate tax exemption options

One of the most important Hong Kong corporate tax exemption mechanisms is the offshore profits exemption. To qualify, companies must demonstrate that profit-generating activities take place outside Hong Kong and that sufficient operational substance exists offshore.

Dividend income is generally not taxable, and capital gains are usually excluded from profits tax if they are capital in nature. Royalty income, however, may be taxable when it is connected to the use of intellectual property in Hong Kong, depending on the specific facts and assessment principles.

How to calculate tax using the Hong Kong corporate tax calculator

Calculating profits tax accurately is an important part of managing compliance and cash flow. While professional tax advice is recommended for complex cases, a Hong Kong corporate tax calculator can be a useful tool for estimating tax liabilities based on the applicable Hong Kong corporate tax rate.

Steps to compute assessable profits

To arrive at assessable profits, businesses generally follow these steps:

- Determine gross profits, based on total revenue minus direct costs of sales.

- Subtract allowable deductions, including operating expenses such as rent, employee costs, professional fees, and marketing expenses.

- Deduct depreciation allowances, also known as capital allowances, on qualifying machinery and capital assets.

- Adjust for non-deductible expenses, such as private expenses, non-business-related costs, and capital expenditures not eligible for allowances.

- Arrive at assessable profits, which form the basis for applying the relevant tax rates.

Using a Hong Kong corporate tax calculator for estimation

A Hong Kong corporate tax calculator is commonly used to forecast profits tax payable and support quarterly or annual cash flow planning. It allows businesses to estimate tax exposure early and make informed budgeting decisions.

Typical inputs for a calculator include total revenue, deductible business expenses, depreciation or capital allowances, and any applicable tax incentives. Based on these inputs, the calculator applies the relevant Hong Kong corporate tax rate, including the two-tiered system where applicable, to generate an estimated tax amount.

However, they cannot assess complex issues such as offshore profits exemption claims, transfer pricing adjustments, or special tax rulings issued by the Inland Revenue Department. As a result, calculator outputs should be treated as indicative estimates rather than final tax liabilities, especially for companies with cross-border operations or specialised tax positions.

Filing requirements and Hong Kong corporate tax return due date

Complying with filing obligations is a key part of managing corporate income tax in Hong Kong. The Inland Revenue Department (IRD) operates a structured and deadline-driven profits tax filing system, and failure to meet these requirements can lead to penalties and increased scrutiny.

Profits tax return issuance and deadlines

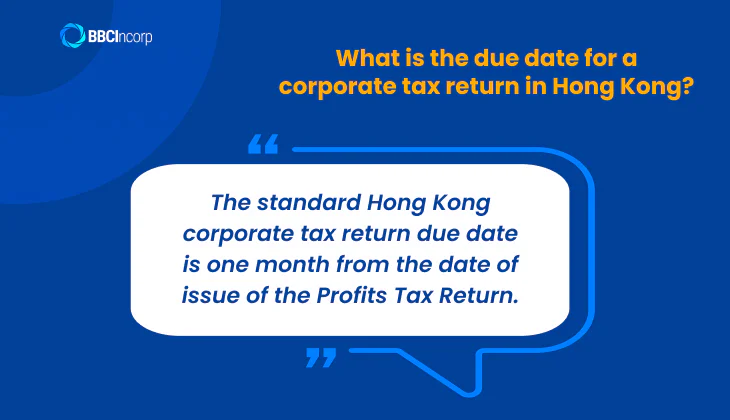

Each year, the Inland Revenue Department (IRD) issues the Profits Tax Return (PTR) to companies, typically around 1 April. Under standard rules, the Hong Kong corporate tax return must be filed within one month from the date of issue, making it critical for businesses to closely monitor the Hong Kong tax filing deadline to avoid penalties.

However, filing deadlines may be extended under the IRD’s administrative concession system, commonly known as the D, M, and N code categories, which align filing deadlines with a company’s accounting year-end. These extensions mainly apply to companies using tax representatives and audited accounts.

For newly incorporated companies, the first profits tax return is generally issued about 18 months after incorporation. This initial return may cover a longer accounting period, and companies should prepare early to ensure timely compliance.

Required documents for tax filing

When filing a profits tax return, companies are typically required to submit:

- Audited financial statements

- Auditor’s report

- Profits tax computation

- Supporting schedules and explanatory notes

If the company is claiming offshore profits exemption or applying specific tax incentive schemes, additional documentation may be required to substantiate the claim, such as contracts, operational records, and functional analyses.

Late filing penalties and compliance consequences

Late or non-filing of profits tax returns can result in additional tax assessments, penalty charges, and fines. In serious cases, the IRD may issue a court summons against the company or its responsible officers.

Beyond immediate penalties, poor compliance history may increase the likelihood of future audits and more detailed reviews, particularly for offshore profits exemption claims. Timely and accurate filing is therefore critical to maintaining a strong compliance profile in Hong Kong.

Common corporate tax challenges and IRD considerations

Navigating Hong Kong corporate tax can be challenging, particularly for businesses with cross-border operations or digital business models. The Inland Revenue Department (IRD) places strong emphasis on substance and supporting evidence, especially where companies seek preferential treatment or claim exemptions.

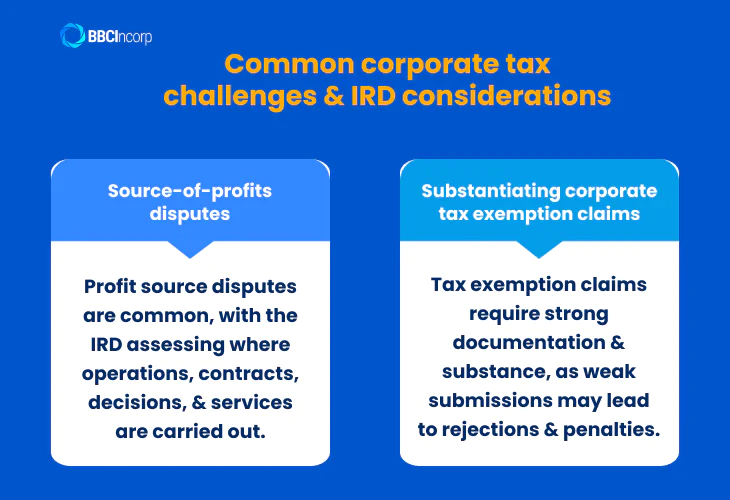

Source-of-profits disputes

One of the most common areas of dispute relates to the determination of profit source. This is particularly complex for service-based businesses, e-commerce platforms, and companies involved in cross-border transactions. In such cases, income generation often spans multiple jurisdictions, making it difficult to clearly identify where profits arise.

The IRD typically focuses on where core operations are carried out, where contracts are negotiated and executed, and where key commercial decisions are made. For service income, the physical or operational location where services are performed is often decisive.

For trading and digital businesses, the IRD may also examine logistics arrangements, platform management, and control over pricing and customer relationships.

Substantiating corporate tax exemption claims

Claiming a Hong Kong corporate tax exemption, particularly under the offshore profits exemption regime, requires robust documentation and clear factual support. Companies are expected to maintain comprehensive records that demonstrate where profit-generating activities take place.

In addition, the IRD increasingly considers economic substance, including the presence of qualified personnel, decision-making authority, and operational control in the relevant jurisdiction. Incomplete, inconsistent, or poorly prepared submissions can lead to rejection of exemption claims, additional tax assessments, and penalties.

Errors in documentation or misrepresentation of facts may also trigger deeper audits and future scrutiny. As a result, companies should approach exemption claims cautiously and ensure that all filings accurately reflect their actual business activities and operational substance.

BBCIncorp’s tax support for Hong Kong companies

Corporate tax advisory and profit calculation support

Managing corporate income tax in Hong Kong requires accurate calculations, timely filings, and robust supporting documentation. Through its integrated accounting services in Hong Kong, BBCIncorp provides comprehensive tax support to help companies remain compliant while optimising their tax position under the applicable Hong Kong corporate tax rate.

Hong Kong tax filing, audit coordination, and compliance services

BBCIncorp assists businesses in preparing accurate profits tax computations based on their actual operations, including:

- Coordinating the preparation of audited financial statements

- Compiling profits tax returns and supporting schedules

- Managing PTR deadlines and applying for filing extensions

- Handling communication and follow-ups with the IRD

Offshore tax exemption assessment and documentation preparation

For companies seeking offshore tax treatment, BBCIncorp provides structured guidance on eligibility assessment under Hong Kong’s territorial tax system. The team assists in preparing detailed substantiation files, including operational analysis and supporting documentation, to support offshore profits exemption claims.

Where reviews or enquiries arise, BBCIncorp helps businesses respond effectively and defend their position during IRD assessments. This comprehensive support allows companies to manage tax obligations confidently while focusing on their core business activities.

Hong Kong continues to be a preferred destination for regional business expansion due to its competitive Hong Kong corporate tax rate, clear territorial tax system, and practical incentives for companies at different growth stages. When understood and applied correctly, businesses can manage tax exposure efficiently while maintaining transparency and predictability.

BBCIncorp supports businesses in navigating Hong Kong corporate tax matters, from tax computation and filing to offshore exemption assessment and IRD communication. With expert support, companies can optimize their tax position, remain fully compliant, and focus on building long-term success in Hong Kong.

Frequently Asked Questions

How much is corporation tax in Hong Kong?

The Hong Kong corporate tax rate follows a two-tiered profits tax system. For corporations, the first HKD 2 million of assessable profits is taxed at 8.25%, while profits above this threshold are taxed at the standard rate of 16.5%. This structure helps reduce the tax burden for small and medium-sized enterprises while keeping corporate income tax in Hong Kong competitive by regional and global standards.

Is Hong Kong a tax haven?

Hong Kong is often described as tax-friendly, but it is not a tax haven. It has a transparent and well-regulated tax system with clear laws, reporting requirements, and active enforcement by the Inland Revenue Department. While the Hong Kong corporate tax rate is low and there are legitimate exemption regimes, companies must meet substance and documentation requirements to benefit. Hong Kong complies with international tax standards and information exchange frameworks.

Does Hong Kong have a territorial tax system for corporations?

Yes. Hong Kong applies a territorial tax system for corporations. Under this system, only profits arising in or derived from Hong Kong are subject to profits tax. Offshore income may qualify for exemption if the company can substantiate that profit-generating activities take place outside Hong Kong. This principle is a core feature of Hong Kong corporate tax and is formally adopted by the IRD.

Disclaimer: While BBCIncorp strives to make the information on this website as timely and accurate as possible, the information itself is for reference purposes only. You should not substitute the information provided in this article for competent legal advice. Feel free to contact BBCIncorp’s customer services for advice on your specific cases.

Industry News & Insights

Get helpful tips and info from our newsletter!

Stay in the know and be empowered with our strategic how-tos, resources, and guidelines.