Delaware Limited Partnership’s formation is a convenient and affordable option for businesses. While general partnerships are often coveted for their general lack of stringent compliance and operational freedom, as businesses grow, partnerships often transition to LLPs or LLCs.

However, for those seeking capital without compromising ownership, a Delaware LP is a good middle-ground. In this article, we’ll discuss the steps of Delaware LP formation and what you need to do after that.

What is a Delaware Limited Partnership?

Delaware Limited Partnerships (DLPs) are a type of business entity in the United States. They are formed by filing a certificate of limited partnership with the Delaware Secretary of State.

What is a Delaware limited partnership

DLPs have two types of partners: general partners and limited partners. General partners manage the business’s day-to-day operations and are liable for its debts. Limited partners are only liable for the amount they invested in the business and do not take part in its management.

DLPs offer several advantages over other types of business entities.

Personal asset protection for limited partners.

Pass-through taxation

The general partner has total authority over the organization and its assets.

Passive investors have high investment potential. Long-term rental income is included in investment possibilities.

Heirs can be paid without receiving the assets. This decreases the estate tax repercussions while maintaining the revenue stream.

Understanding the Delaware Limited Partnership Act

The Delaware Revised Uniform Limited Partnership Act (DRULPA), also known as the Delaware Uniform Limited Partnership Act, is the core legislation that governs how limited partnerships (LPs) are structured and managed in Delaware. Recognized for its clarity and flexibility, DRULPA provides investors and business owners with a modern legal framework that accommodates diverse business needs, from venture capital funds to family estate structures.

It outlines the rights and duties of general and limited partners, establishes rules for management and liability, and defines how profits, losses, and obligations are shared among them.

General Partnership vs Limited Partnership

To understand the essence of a Delaware Limited Partnership, it’s crucial to first look at how it differs from a General Partnership (GP). At the foundation, both General Partnerships (GPs) and Limited Partnerships (LPs) are collaborative business structures involving two or more partners.

However, the Delaware law distinguishes them based on management control and liability exposure – two elements that directly affect how investors participate and how their risks are protected under DRULPA.

Both General Partnerships (GP) and Limited Partnerships (LP) share similar foundations but differ in partner roles and liability.

General Partnership (GP): Governed by the Delaware Revised Uniform Partnership Act (DRUPA).

Limited Partnership (LP): Governed by the Delaware Revised Uniform Limited Partnership Act (DRULPA).

Aspect

General Partnership (GP)

Limited Partnership (LP)

Partners

General partners only

At least one general partner and one limited partner

Liability

Unlimited for all partners

Limited partners’ liability capped at their agreed contribution

Management

Shared by all general partners

Managed by general partners; limited partners do not manage day-to-day

Legal Basis

DRUPA

DRULPA

Important nuance: A limited partner generally maintains limited liability when not participating in control. If a limited partner takes part in control and a third party reasonably believes they are a general partner, limited liability protection may be jeopardized.

Optional structure: A Limited Liability Limited Partnership (LLLP) is available in Delaware. When properly formed, it can extend limited liability protection to the general partner.

Roles and Responsibilities

Under DRULPA, each partner’s role is clearly defined to ensure smooth management and accountability within the partnership. The distinction between general and limited partners also determines their exposure to liability and their influence in business decisions.

General Partners: Run daily operations, make strategic and financial decisions, and bear personal liability for partnership obligations.

Limited Partners (often “silent” partners): Contribute capital, receive economic rights, and do not manage operations. They retain limited liability so long as they avoid participating in control.

These defined responsibilities form the operational backbone of every Delaware LP. Understanding them lays the groundwork for how profits and taxes will be allocated among partners.

Tax Treatment

Delaware partnerships are typically treated as pass-through entities for tax purposes. Income, losses, deductions, and credits flow through to the partners and are taxed once at the partner level, rather than at both the entity and partner levels.

This pass-through tax structure makes Delaware LPs especially attractive for investors seeking efficient profit distribution and minimal double taxation. However, to formalize how profits and responsibilities are shared, a written Partnership Agreement is indispensable.

Partnership Agreement

The Partnership Agreement is the central document that governs the internal affairs of a Delaware LP. Although not required to be filed with the State, it serves as the binding contract that aligns the rights, obligations, and expectations of all partners.

Every Delaware LP operates under a Partnership Agreement. It does not need to be filed with the State and should clearly set out:

Partner roles, rights, and admission or withdrawal mechanics

Management structure and decision-making rules

Profit and loss allocations and distributions

Capital contributions and calls

Transfer restrictions and buy-sell terms

Dispute resolution procedures

Delaware limited partnership agreement

Ultimately, DRULPA and the Partnership Agreement work hand in hand to provide Delaware LPs with both legal stability and operational flexibility making them one of the most efficient partnership structures available in the U.S.

What is the aim of Limited Partnerships?

Under the Delaware Limited Partnership Act, Limited Partnerships are most commonly established for two primary purposes:

Under the Delaware Limited Partnership Act, Limited Partnerships (LPs) are typically formed to facilitate investment and management efficiency. Their flexible structure allows investors to pool capital while maintaining limited liability and clear management separation.

In practice, Delaware LPs are most commonly established for two main purposes:

To build commercial real estate projects

The limited partner is responsible for capital investment, while the general partner is in charge of project management and construction. Once completed the limited partner receives a return on the completed project’s income stream, such as rental revenue or profit distribution.

The limited partner functions as a passive investor in this case. A limited partnership can manage and build projects such as apartment complexes and shopping malls.

To make use of an estate-planning vehicle

The limited partners act as the general partners’ successors, whereas the general partners are the parents who own the real estate. Typically, the assets involved include commercial or investment real estate.

This kind of limited partnership, also known as a Family Limited Partnership, is most advantageous when the limited partnership’s asset generates an income stream and the parties involved do not want the asset to be sold following the death of the general partner.

Limited partnerships were also a popular choice for filmmakers when there was no LLP or LLC yet. Directors valued their creative freedom above all else, which could easily be compromised in an LLC or LLP as there are other stakeholders in the mix.

A limited partnership allows for passive funding from relatives and family members to help directors get their projects off the ground while still retaining full creative control.

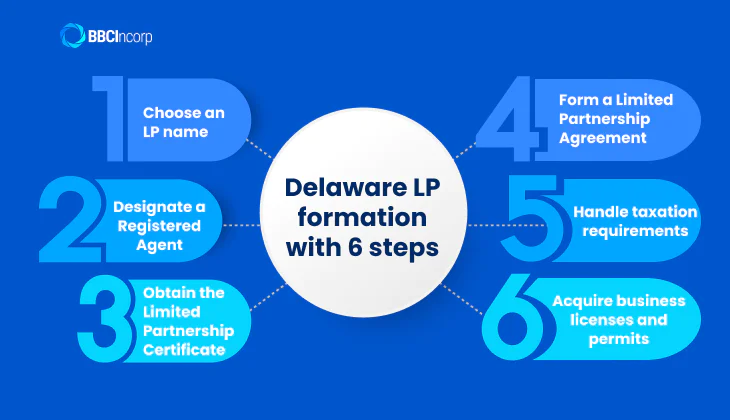

Delaware LP formation with 6 steps

Step 1: Choose an LP name

The Delaware Limited Partnership Act (DLPA) requires that all LPs formed in Delaware have a distinctive name. The name must include the words “Limited Partnership” or the abbreviation “L.P.” It cannot be the same as the name of any other business entity registered with the Delaware Division of Corporations.

There are some additional considerations to take into account when choosing an LP name. The name should be easy to remember and spell. It should also be reflective of the business’s purpose. For example, a Delaware LP formed to invest in real estate might choose a name like “Delaware Real Estate Limited Partnership.”

Once you have chosen an appropriate name for your company, you will need to file paperwork with the Delaware Division of Corporations. By that time, this will officially register your LP and allow you to begin doing business in Delaware.

Step 2: Designate a Registered Agent

Delaware LP formation requires that you designate a Registered Agent. So that is an individual or business entity that agrees to accept legal papers on behalf of your company.

Without a registered agent in Delaware, you risk losing your good standing, and the state has the authority to dissolve your LP if they so want. In the worst-case scenario, the state may fail to notify you of a lawsuit filed against your firm.

Step 3: Obtain the Limited Partnership Certificate

To legalize your limited partnership, you need to file the Delaware Limited Partnership Certificate of Formation. The document is very simple to complete and simply needs the information shown below:

The limited partnership’s name

The limited partnership’s address

Each general partnership’s name and mailing address

Signature of an authorized person

Online PDF versions of the Certificate of limited partnership Delaware can be filled out and sent to the Delaware Division of Corporations via mail.

Processing Time: The Certificate of Limited Partnership document is not subject to a set processing period according to Delaware law.

Step 4: Form a Limited Partnership Agreement

A Delaware Limited Partnership agreement describes some of the important company operating principles, even though the state does not legally require it of Delaware. It is a crucial document that outlines the specifics of the agreement between the general partners and limited partners, even if you are not required to submit it to the state to establish your limited partnership (LP).

Depending on your company’s size, industry, and other variables, the information contained in a limited partnership agreement can change. Generally speaking, it’s a good idea to document the following details:

The period of your partnership (in years)

Identities and roles of general and limited partners

Initial capitalization and ongoing capital contributions

Profit/loss distribution

Structure of management

Voting rights and meeting plans

Accounting and record-keeping practices

Conditions for transfer and dissolution

Step 5: Handle taxation requirements

When you form a Delaware LP, you’ll need to handle the taxation requirements. Delaware has a corporate income tax, but LPs are exempt from this tax. However, you will still need to pay taxes on any profits that your LP earns.

Having 2 levels of taxation requirements: State level and Federal level.

Step 6: Acquire business licenses and permits

You can apply for Delaware licenses and permits online through the state’s One Stop Business Registration and Licensing system.

It is also important to check with local authorities in case there are additional licenses or permits required for specific counties or municipalities. For example, if you plan on serving food at your business, it may require a special permit from the local health department.

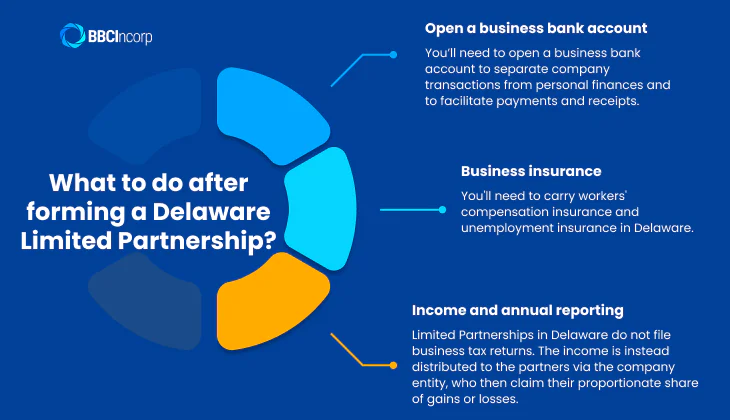

What to do after forming a Delaware Limited Partnership?

Once your Delaware Limited Partnership (LP) is successfully formed, there are several key steps to complete before it can operate smoothly and remain compliant.

Open a business bank account

You’ll need to open a business bank account to separate company transactions from personal finances and to facilitate payments and receipts.

However, opening a U.S. business account can be challenging for non-residents, as many traditional banks remain cautious due to anti-money-laundering (AML) regulations and tend to restrict foreign applications.

A better alternative is to just open an offshore bank account where the regulations play in your favor or you can even give neobanks a try if you need to register an account fast. Give our banking tool a try to find the right banking solution for your business.

At BBCIncorp, we provide support for business bank accounts and payment setup. Our dedicated team connects you with a world of trusted banks and payment services, ensuring you find the perfect fit for your business needs.

Business insurance

You’ll need to carry workers’ compensation insurance and unemployment insurance in Delaware. General liability insurance is also required, as well as some industry-specific policies.

The state’s One Stop Business Registration and Licensing system can help you find the right insurance for your business.

Income and annual reporting

Limited Partnerships in Delaware do not file business tax returns. The income is instead distributed to the partners via the company entity, who then claim their proportionate share of gains or losses. Still, LPs do need to file an annual information return with the IRS for the year.

Limited Partnerships in Delaware, unlike in many other states, are not obliged to file any form of an annual report to maintain good standing with the state.

What to do after forming a delaware limited partnership

COMPLYMATE

Tired of sifting through endless paperwork to understand jurisdictions’ compliance requirements? Our guide can help!

Delaware Limited Partnership Formation Service at BBCIncorp

Setting up a company in Delaware offers business owners access to one of the most stable and flexible corporate frameworks in the United States. However, navigating formation procedures, tax registration, and ongoing compliance can be complex, especially for non-residents unfamiliar with U.S. requirements.

This is where BBCIncorp makes a difference. With more than a decade of experience supporting thousands of global entrepreneurs, we provide end-to-end solutions that simplify every step of your Delaware company formation.

Why choose BBCIncorp for your Delaware company setup?

End-to-end service with full compliance

From company registration and registered agent services to EIN application and banking setup, BBCIncorp ensures a seamless and fully compliant process under Delaware and U.S. law.

Transparent pricing with no hidden costs

All service fees are clearly outlined, helping you plan your budget with complete confidence and no unexpected expenses.

Expert guidance and global support

Our multilingual specialists and international partner network deliver professional support throughout your business lifecycle, from incorporation to ongoing compliance.

Delaware is one of the most popular states in which to form a delaware limited partnership (LP) because it offers many advantages to businesses, including a well-developed court system and favorable business laws.

If you have any questions about the process or want help setting up your company, feel free to email service@bbcincorp.com. We would be happy to assist you in any way we can.

Frequently Asked Questions

Can a Delaware limited partnership have only one partner?

Delaware limited partnerships can have one or more partners. It must have at least two partners, but there is no maximum number of partners.

What is the difference between LLC and LP?

One key difference between LLCs and LPs is that an LLC offers limited liability protection for its members, while an LP does not. This means that if your company is sued, the members’ personal assets cannot be seized to pay off any judgments against the company.

Does a Delaware LP have legal personality?

Delaware LP does have legal personality. Limited partnerships are unique in that they have two levels of existence – the general partnership and the limited partnership. The limited partnership is a separate entity from its partners and can own property, enter into contracts, and sue or be sued.

Why would you choose LP over LLC?

Delaware Limited Partnerships offer more limited liability protection than Delaware LLCs. In the event that a lawsuit is filed against the partnership, the partners’ personal assets cannot be used to satisfy any judgment obtained against the business. This is not the case with LLCs – the owners of an LLC can be held liable for business debts and judgments.

Disclaimer: While BBCIncorp strives to make the information on this website as timely and accurate as possible, the information itself is for reference purposes only. You should not substitute the information provided in this article for competent legal advice. Feel free to contact BBCIncorp’s customer services for advice on your specific cases.