Table of Contents

Understanding “what is equity in accounting” starts with a simple truth: equity represents what a business truly owns after settling its obligations, and it sits at the heart of every sound financial statement. Whether you’re a business owner tracking growth, an investor assessing value, or an accountant preparing reports, understanding accounting equity meaning is non-negotiable.

At its core, equity is defined by a simple but powerful relationship: Assets − Liabilities = Equity. This foundational accounting equation tells you exactly how much of a company’s resources belong to its owners or shareholders after debts are accounted for.

Owner’s equity and shareholder equity appear across key financial statements, from the balance sheet to the statement of changes in equity, giving stakeholders a clear window into financial health, business valuation, and long-term growth potential.

In this guide, we’ll break down what equity in accounting really means, how to calculate it, and why it matters at every stage of your business journey.

Key Takeaways:

- Equity in accounting represents the residual value of a business after liabilities are deducted from assets, reflecting true ownership value.

- The core formula Equity = Assets − Liabilities is fundamental to understanding financial position and business valuation.

- Key components include share capital, retained earnings, and distributions, each directly impacting how equity grows or declines over time.

- Equity provides critical insights into financial health, helping investors and owners assess profitability, stability, and long-term growth potential.

- Maintaining accurate equity records and leveraging professional accounting support ensures reliable reporting and better strategic decision-making.

What is equity in accounting?

Equity in accounting is defined as the residual interest in a business’s assets after all liabilities have been deducted. Simply put, it represents what would remain for the owners if the company sold everything it owned and settled every debt. This makes equity synonymous with a business’s net worth – the true ownership value from the owner’s perspective.

Everything the company owns (assets), minus everything it owes (liabilities), equals the owner’s or shareholders’ claim on the business.

You’ll encounter this figure under several names, depending on the business structure, owner’s equity, shareholder equity, or net assets. But they all refer to the same underlying concept. Equity appears prominently on the balance sheet, where it provides a point-in-time snapshot of ownership value.

How equity looks in practice depends on business type:

- Sole proprietorship: Equity reflects the single owner’s capital contributions plus accumulated profits, minus any drawings.

- Partnership: Equity is split across multiple partners’ capital accounts, each representing their proportional stake.

- Corporation: Shareholder equity includes paid-in capital, retained earnings, and may be reduced by treasury stock or dividends paid out.

Equity can be positive (assets exceed liabilities), negative (liabilities exceed assets), or zero, and each scenario tells a different story about a business’s financial standing.

Why equity matters for businesses?

Equity isn’t just an accounting line item; it’s one of the most telling indicators of a business’s financial health and long-term sustainability.

A growing equity balance generally signals that a business is profitable and managing its finances well. Declining equity, on the other hand, can be an early warning sign worth investigating before it becomes a deeper problem.

Here’s why tracking equity has real business equity value across key decisions:

- For investors, equity reveals how much of the business current owners hold and helps determine what the company is actually worth. Strong equity makes a business significantly more attractive when seeking investment, and directly influences how shares are valued.

- For lenders and banks, equity is a critical factor before approving loans or extending credit. Higher equity signals lower lending risk; it demonstrates that owners have meaningful “skin in the game.” This can not only improve your chances of securing finance but also lead to more favorable loan terms, strengthening your overall financial plan.

- For business owners, equity importance in accounting goes beyond compliance. It shapes your negotiating position in a potential sale, influences your ability to raise capital, and reflects whether the business can sustain growth without over-relying on debt.

In short, equity sits at the intersection of valuation, funding, and strategic planning. Whether you’re preparing for investment, applying for a loan, or planning an exit, a clear picture of your equity position is non-negotiable.

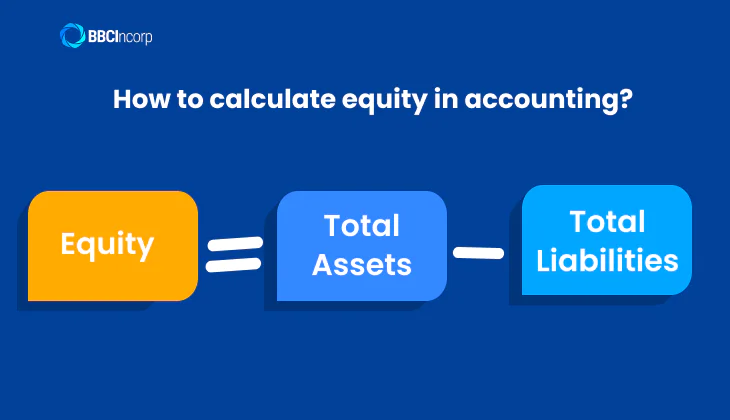

How to calculate equity in accounting?

Calculating equity in accounting is more straightforward than it might seem. The equity formula accounting professionals use every day comes directly from the core accounting equation:

Assets = Liabilities + Equity

Rearranged to solve for equity:

Equity = Total Assets − Total Liabilities

To apply this formula, you need to understand what goes into each component:

- Assets: everything your business owns or is owed: cash, inventory, equipment, property, and accounts receivable.

- Liabilities: everything your business owes: supplier invoices, bank loans, employee wages payable, and tax obligations.

- Equity: the residual value that belongs to the owner(s) once all liabilities are settled.

Here’s how to calculate equity in accounting for a small business:

- Step 1: Add up all your assets

- Step 2: Add up all your liabilities

- Step 3: Subtract total liabilities from total assets

Worked example:

Imagine you run a small bakery. You own commercial baking equipment worth $40,000, have $15,000 cash in the bank, and customers owe you $5,000 in outstanding orders, bringing your total assets to $60,000. On the other side, you have a $20,000 equipment loan and $8,000 in unpaid supplier bills, making your total liabilities $28,000.

| Item | Amount (USD) |

| Total Assets (equipment, cash, receivables) | $60,000 |

| Total Liabilities (loan, supplier payables) | $28,000 |

| Total Equity | $32,000 |

This $32,000 is the owner’s net stake in the bakery at that point, the amount that would remain if every liability were settled today.

Several factors can shift this figure in financial reporting, including changes in retained earnings, additional capital contributions, dividend payments, and fluctuations in asset values or outstanding debt.

Regardless of business structure (sole proprietorship, partnership, or corporation), the underlying equity formula stays the same. What changes is simply how equity is labeled and broken down within the balance sheet.

Breaking down the components of equity

Equity isn’t a single fixed number; it’s built from several moving parts, each reflecting a different aspect of how value flows in and out of a business. Here’s what makes up the components of equity in accounting:

Owner’s capital or contributed capital

This is the money owners or shareholders put into the business, the foundational investment that gets operations off the ground. Any additional funds contributed later also add to this figure.

In corporations, this takes the form of share capital, recorded as common stock at par value, with any amount paid above that recorded as additional paid-in capital. In sole proprietorships and partnerships, it’s simply tracked as the owner’s or partners’ capital accounts.

Retained earnings

Retained earnings represent the cumulative profits a business has kept rather than distributed to owners. Every time the business turns a profit and reinvests it, instead of paying it out, retained earnings grow, and so does total equity.

The reverse is also true: net losses erode retained earnings, directly reducing equity. This makes retained earnings a reliable indicator of how well a business generates and preserves value over time. Strong retained earnings signal financial self-sufficiency, the ability to fund expansion or repay debt without relying on external financing.

Distributions, drawings, and dividends

These represent value leaving the business for its owners, and they reduce equity accordingly:

- In sole proprietorships and partnerships, owner withdrawals are called drawings

- In corporations, profits paid out to shareholders are called dividends

Regardless of structure, every distribution lowers the equity balance, the mirror image of a capital contribution.

Other equity components

Larger or more complex businesses may carry additional equity items:

- Treasury stock: shares repurchased by the company from the open market, which reduces total shareholders’ equity

- Preferred stock: a separate class of share capital with distinct rights, such as priority dividend payments

- Accumulated Other Comprehensive Income (AOCI): unrealized gains or losses not yet reflected in the income statement, such as foreign currency adjustments or certain investment changes

Together, these components paint a complete picture of shareholder equity, not just what’s been earned, but how it’s been built, retained, and distributed over time.

Equity vs owner’s equity vs net worth

Although often used interchangeably, these accounting equity terms have slightly different applications depending on context and business structure.

At its core, equity refers to the residual value of a business after liabilities are deducted from assets. It is a broad term used across all types of entities. In practice, owner’s equity is simply equity viewed in the context of a sole proprietorship or partnership, highlighting the owner’s direct claim on the business.

Meanwhile, net worth is a more general term, commonly used outside formal accounting. It represents the same concept, what remains after all debts are paid, but can apply to both businesses and individuals. This is why comparisons like owner’s equity vs net worth often reveal that they are conceptually identical, but used in different settings.

The terminology also shifts in corporations, where equity is typically called shareholder equity to reflect multiple owners.

For example, if a business has $500,000 in assets and $300,000 in liabilities, its equity (or owner’s equity/net worth) is $200,000. Whether you call it equity, owner’s equity, or net worth depends on whether you’re discussing a company, a sole trader, or personal finances, but the underlying calculation remains the same.

| Term | Definition | Common Usage Context | Key Difference |

| Equity | Residual value after liabilities are deducted from assets | All business structures | Broad, standard accounting term |

| Owner’s Equity | Equity belonging to a single owner or partners | Sole proprietorships & partnerships | Emphasizes ownership in non-corporations |

| Net Worth | Total assets minus total liabilities (individual or business) | Personal finance & general discussions | More informal, widely used outside accounting |

Equity on the balance sheet: What to look for

Equity on the balance sheet is presented as a distinct section, typically following assets and liabilities. It completes the accounting equation and shows the net value attributable to owners or shareholders. Understanding this section is essential when analysing a shareholder equity statement and overall financial health.

Common items found in the equity section include:

- Share capital: funds raised from issuing shares

- Retained earnings: accumulated profits kept in the business

- Additional paid-in capital: excess paid above share par value

- Reserves: gains or adjustments not reflected in net income

Rather than viewing equity in isolation, it should always be assessed alongside assets and liabilities. A positive and growing equity balance indicates that the company is generating value and maintaining financial stability. In contrast, negative equity may signal financial distress or excessive debt.

For investors and managers, equity provides insights into profitability, reinvestment strategy, and risk level. Tracking changes in equity over time helps evaluate business performance, understand funding decisions, and identify whether growth is driven by operations or external capital.

Equity financing: using equity to raise capital

Equity financing business refers to raising capital by selling ownership stakes to investors instead of borrowing money. In this model, companies issue shares, such as common or preferred stock, in exchange for cash, which increases both assets and total equity on the balance sheet.

This approach is widely used by startups and high-growth companies seeking funding without taking on repayment obligations.

Compared to debt financing, equity financing does not require fixed interest payments or repayment schedules. While debt preserves ownership, it increases financial risk through liabilities. In contrast, equity investment spreads risk across investors but involves sharing future profits and decision-making power.

For startups, equity financing offers several advantages. It provides access to capital without immediate cash flow pressure, making it easier to invest in product development, hiring, and market expansion. In addition, investors, such as venture capital firms or angel investors, often bring strategic guidance, networks, and credibility.

However, the trade-off is ownership dilution. Founders must give up a portion of control and future earnings. As more funding rounds occur, their stake may decrease significantly. Therefore, businesses must carefully balance the need for capital with long-term ownership and control considerations.

Understanding negative equity

Negative equity accounting occurs when a company’s total liabilities exceed its total assets, resulting in a negative net value. In simple terms, the business owes more than it owns, which signals financial imbalance.

This situation often arises from accumulated losses over time, excessive borrowing, or a decline in asset value. For example, consistent operating losses reduce retained earnings, while taking on too much debt increases liabilities, both contributing to negative equity.

Negative equity has serious implications for financial stability. It can reduce investor confidence, limit access to new financing, and raise concerns about the company’s ability to continue operating. Lenders and investors may view it as a sign of high risk or potential insolvency.

However, negative equity does not always mean immediate failure. Businesses can recover by improving profitability, restructuring debt, or securing new capital. Monitoring this condition early allows companies to take corrective action before it escalates into a more critical financial issue.

The equity method of accounting

The equity method of accounting is applied when a company owns a significant but non-controlling stake (typically 20%–50%) in another business. At this level, the investor can influence decisions but does not fully control operations.

Instead of keeping the investment at its original cost, the value is updated over time based on performance:

- Profit from investee → increase investment value

- Loss from investee → decrease investment value

- Dividends received → reduce investment value (not recorded as income)

Simple example: A technology company invests 25% in a startup.

- The startup earns $200,000 → the investor records $50,000 income (25%) and increases the investment value.

- Later, the startup pays $20,000 dividends → the investor reduces the investment value by $5,000 (25%).

This method reflects the real economic relationship; your returns depend on how well the investee performs, not just the initial purchase price.

Common equity mistakes and how to avoid them

Understanding equity is one thing; applying it correctly is another. Below are common accounting mistakes in equity, explained with clear, practical examples.

Messy record-keeping

Poor tracking of capital and withdrawals leads to unreliable equity figures.

Example:

A founder invests $50,000 but forgets to record an additional $10,000 later. Equity appears lower than it actually is.

Fix: Use consistent bookkeeping and update records in real time.

Mixing personal and business finances

Unclear boundaries distort both profit and equity.

Example:

Paying personal rent from the business account without recording it as drawings reduces equity incorrectly.

Fix: Separate accounts and label every transaction clearly.

Misunderstanding profit vs equity

Profit is a period result; equity is a cumulative value.

Example:

A business earns $30,000 profit but distributes $25,000 as dividends. Equity only increases by $5,000, not $30,000.

Fix: Focus on retained earnings, not just profit.

Incorrect valuation of assets or liabilities

Wrong valuations can mislead stakeholders.

Example:

Overstating inventory value inflates total assets → equity appears stronger than reality.

Fix: Regularly review valuations and ensure liabilities are fully recorded.

BBCIncorp’s professional accounting services for accurate equity management

Maintaining accurate equity records is essential for understanding true business value, yet it can quickly become complex without the right expertise. Professional accounting services play a critical role in ensuring that equity is calculated correctly and consistently reflected across financial reports.

Experienced accountants help businesses manage key areas such as balance sheets, financial statements, and shareholder records. This includes tracking capital contributions, monitoring ownership changes, and ensuring retained earnings are accurately recorded over time.

With reliable bookkeeping services, companies can clearly see how profits, losses, and distributions impact their overall equity position.

BBCIncorp offers tailored accounting solutions designed for startups, SMEs, and international businesses. Our services support companies in maintaining structured financial records while navigating different regulatory environments.

Working with professional accountants brings several advantages:

- Accurate bookkeeping and reporting: Clear, audit-ready financial data

- Compliance assurance: Alignment with international accounting standards

- Strategic insights: Better visibility into financial performance and growth opportunities

By combining technical expertise with practical business understanding, BBCIncorp helps companies build a strong financial foundation, ensuring equity is not only accurate but also actionable for decision-making.

Conclusion

This “what is equity in accounting” guide highlights that equity is more than just a number; it represents the true ownership value of a business. From contributed capital to retained earnings, each component plays a role in shaping financial position and long-term growth.

Understanding and tracking business equity is essential for accurate financial reporting, informed decision-making, and sustainable expansion. It helps business owners and investors evaluate performance, manage risks, and plan for the future with confidence.

However, maintaining precise equity records requires consistency and expertise. As businesses grow and financial structures become more complex, professional support becomes increasingly valuable. By leveraging reliable accounting services, companies can ensure their equity is accurately managed, turning financial data into a powerful tool for strategic growth.

Frequently Asked Questions

Is equity the same as capital?

No. Capital refers to the money or assets invested in a business, while equity is the remaining value after all liabilities are deducted. In simple terms, capital contributes to equity, but they are not the same.

What is the formula for determining equity?

Equity is calculated using the basic accounting equation:

Equity = Assets − Liabilities

This shows what owners actually “own” after all debts are paid.

What are the main components of equity?

Equity typically includes:

- Share capital or owner’s capital (initial and additional investment).

- Retained earnings (accumulated profits).

- Additional paid-in capital.

- Dividends or withdrawals (which reduce equity).

Is equity an asset or a liability?

Neither. Equity represents the owners’ claim on the business after liabilities are settled. It appears as a separate section on the balance sheet.

Can a business have negative equity?

Yes. Negative equity occurs when liabilities exceed assets. It is often caused by ongoing losses or high debt levels and may signal financial risk, but it can be improved with better performance or restructuring.

Disclaimer: While BBCIncorp strives to make the information on this website as timely and accurate as possible, the information itself is for reference purposes only. You should not substitute the information provided in this article for competent legal advice. Feel free to contact BBCIncorp’s customer services for advice on your specific cases.

Industry News & Insights

Get helpful tips and info from our newsletter!

Stay in the know and be empowered with our strategic how-tos, resources, and guidelines.