Table of Contents

The best business bank account for startups and SMEs in Singapore depends on whether your company prioritizes local banking, international payments, multi-currency support, low operating costs, or scalable financial tools.

Traditional banks such as DBS, OCBC, and UOB offer full banking services, while digital providers like Aspire, Airwallex, Wise, YouBiz, and Revolut often provide faster onboarding and lower cross-border transaction costs.

This article reviews the top 10 best business bank accounts in Singapore to help startups, SMEs, local founders, and foreign entrepreneurs compare the right options for their business needs.

Key Takeaways

- Traditional banks are better for businesses needing loans, branch support, cheque alternatives, and long-term banking relationships.

- Digital business accounts are often easier for startups, SMEs, and foreign founders to open remotely.

- Multi-currency capability matters for e-commerce, SaaS, trading, and international service businesses.

- The lowest monthly fee may not be the most cost-effective option after FX, transfer, and fall-below fees.

- Foreign-owned startups should check onboarding rules before incorporation to avoid account-opening delays.

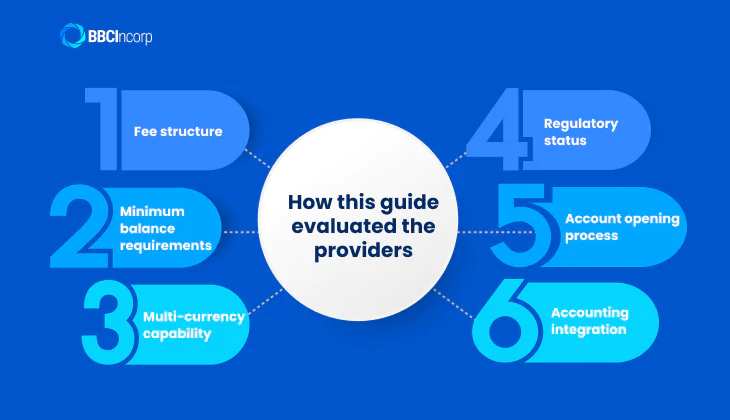

How this guide evaluated the providers

The business bank accounts in this guide were selected based on their market presence in Singapore, relevance to startups and SMEs, and suitability for both local and foreign founders.

We also considered providers that are commonly referenced in high-authority comparison articles and official banking resources as of 2026.

To keep the comparison practical and transparent, each provider was reviewed using the following criteria:

- Fee structure: monthly account fees, fall-below fees, transaction charges, and outward telegraphic transfer costs, based on official provider pricing pages where available.

- Minimum balance requirements: initial deposit, minimum average daily balance, and related fall-below conditions.

- Multi-currency capability: supported currencies, foreign exchange model, and whether international transfers use local payment rails or SWIFT.

- Regulatory status: whether the provider operates as a licensed bank or a digital payment provider, and whether eligible SGD deposits are covered by Singapore Deposit Insurance Corporation (SDIC).

- Account opening process: online application availability, estimated approval timeline, documentation requirements, and suitability for foreign-owned companies.

- Accounting integration: availability of Xero or other accounting software integrations to support bookkeeping and reconciliation.

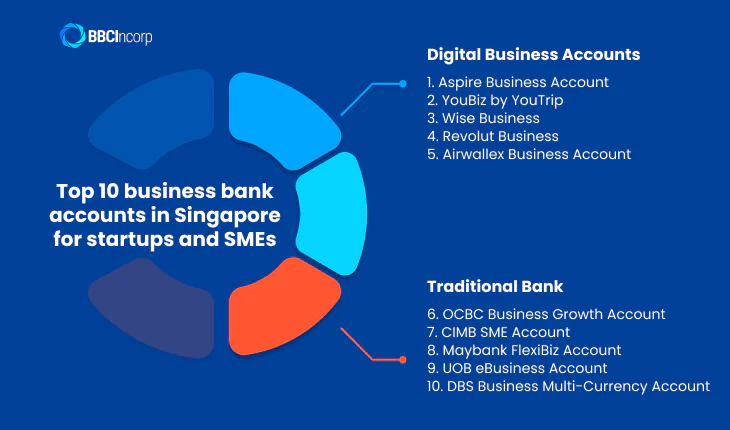

Top 10 business bank accounts in Singapore for startups and SMEs

Singapore startups and SMEs can choose between two broad options: traditional corporate bank accounts and digital business accounts.

Traditional banks are stronger for regulated businesses, loans, and local banking relationships. Digital providers are often more suitable for lean startups, foreign founders, online businesses, and companies with frequent cross-border payments.

| Provider | Type | Best For | Min. Deposit / Balance | Monthly Fee (SGD) | Multi-Currency | Open Remotely |

| Aspire Business Account | Digital business account | Startups, foreign founders, digital SMEs | S$0 | S$0 | Yes, 30+ currencies | Yes, subject to KYC |

| YouBiz by YouTrip | Digital business account | Corporate cards, PayNow collections, overseas spend | No public minimum stated | No monthly fee advertised | Yes, 8 receiving currencies | Yes, subject to KYC |

| Wise Business | Digital business account | International payments and FX | No minimum balance | No monthly fee; one-off setup fee may apply | Yes | Yes, subject to KYC |

| Revolut Business | Digital business account | Global teams and expense management | No public minimum balance | From S$0/month | Yes, 25+ currencies | Yes, subject to KYC |

| Airwallex Business Account | Digital business account | Cross-border payments and e-commerce | No public minimum balance | Free plan available | Yes, 20+ currencies | Yes, subject to KYC |

| OCBC Business Growth Account | Traditional bank | Local SMEs needing bank support | S$1,000 | S$10; waived first 2 months; S$20 fall-below fee | Yes, 13 currencies via linked account | Yes, for eligible businesses |

| CIMB SME Account | Traditional bank | SMEs seeking low balance pressure | Nil for SME/SME-i Account | S$8; waived first 12 months | Separate FCY accounts available | Yes, subject to eligibility |

| Maybank FlexiBiz Account | Traditional bank | Local startups with basic SGD banking | S$1,000 | No monthly fee; S$10 fall-below fee | Separate FCY accounts available | Yes, for eligible local businesses |

| UOB eBusiness Account | Traditional bank | SMEs needing SGD banking and payroll tools | S$1,000 initial; S$5,000 average balance | S$35 annual fee; S$15 fall-below fee | Separate FCY accounts available | Yes, subject to eligibility |

| DBS Business Multi-Currency Account | Traditional bank | SMEs needing traditional multi-currency banking | S$10,000 average balance for standard account | S$10 Starter Bundle; S$50 annual standard fee | Yes, 13 currencies | Yes, for eligible local-owned businesses |

Disclaimer

This summary is based on publicly available provider information as of June 2026 and is intended as a general guide only. Fees, eligibility rules, and product features may change, so readers should verify the latest terms directly with each provider before applying.

Digital Business Accounts

1. Aspire Business Account

Aspire is a digital business account built for startups, SMEs, and fast-growing companies that want online onboarding, corporate cards, expense management, and multi-currency payments.

Aspire states that its Singapore business account has S$0 monthly fees, S$0 initial deposit, S$0 minimum balance, and supports payments in 30+ currencies, with funds safeguarded with DBS Bank and other Tier-1 banks.

BBCIncorp also works with Aspire as part of its banking support network, helping newly incorporated businesses prepare the right documents to open bank accounts for Singapore entities and improve their account-opening readiness.

This is especially useful for foreign founders who may be unfamiliar with Singapore know-your-customer checks.

Pros

- No monthly fee, initial deposit, or minimum balance publicly advertised.

- 100% online application.

- Strong fit for cards, SaaS spending, expense control, and startup operations.

- Xero and other accounting integrations available.

Cons

- Not a traditional deposit-taking bank.

- No physical branch support.

- Account approval remains subject to KYC and business profile checks.

Best for: Startups, foreign founders, digital businesses, and SMEs that want fast onboarding and modern spend management.

| Aspire Quick Facts | Details |

| Best For | Startups, SMEs, foreign founders |

| Min. Balance | S$0 |

| Monthly Fee | S$0 |

| Currencies | 30+ payment currencies |

| FX Rate | Upfront rates and fees |

| SDIC-Insured | No; funds are safeguarded, not treated like bank deposits |

| Remote Opening | Yes, subject to KYC |

| Xero Integration | Yes |

2. YouBiz by YouTrip

YouBiz is a digital business account and corporate card solution from YouTrip’s business arm. It supports multi-currency accounts, PayNow QR, overseas payments, and card spending. YouBiz states that users can receive money in 8 currencies and use a dedicated PayNow QR code for SGD business payments .

You Technologies Group Singapore is licensed under Singapore’s Payment Services Act as a major payment institution, and its terms state that customer monies are held in dedicated segregated customer accounts with safeguarding institutions such as DBS, Standard Chartered, OCBC, and Deutsche Bank Singapore .

Pros

- Useful for corporate cards and overseas spending.

- PayNow QR support for local collections.

- Segregated safeguarding arrangements.

- Xero connection is available through YouBiz support flows.

Cons

- Not a traditional bank deposit account.

- Public pricing details may be less centralized than bank pricing guides.

- Better suited for spend and payment operations than lending needs.

Best for: SMEs and startups with overseas card spending, travel, supplier payments, or team expense needs.

| YouBiz Quick Facts | Details |

| Best For | Card spending, PayNow collections, overseas payments |

| Min. Balance | No public minimum stated; confirm before applying |

| Monthly Fee | No monthly fee advertised for key account use |

| Currencies | 8 receiving currencies; card spend in more currencies |

| FX Rate | YouBiz promotes low or no FX markup for card spend |

| SDIC-Insured | No; safeguarded under payment services framework |

| Remote Opening | Yes, subject to KYC |

| Xero Integration | Yes, via YouBiz-Xero connection |

3. Wise Business

Wise Business is a strong option for companies that receive, hold, convert, and send money internationally. Wise states that Singapore businesses can get Wise Business features for a one-off S$99 setup fee, with low-cost global transfers and transparent conversion fees .

Pros

- Strong FX transparency.

- Good for global collections and supplier payments.

- No traditional monthly account maintenance fee.

- Useful for online businesses and international contractors.

Cons

- Not a traditional Singapore bank account.

- One-off setup fee applies for full business features.

- Xero integration is available, but some Wise-Xero features may vary by market. Singapore businesses should verify which functions are supported before relying on the integration.

Best for: International businesses, freelancers, e-commerce sellers, and companies paid in foreign currencies.

| Wise Quick Facts | Details |

| Best For | International payments and FX |

| Min. Balance | No minimum balance |

| Monthly Fee | No monthly fee; one-off setup fee may apply |

| Currencies | Multi-currency support |

| FX Rate | Mid-market rate plus transparent fees |

| SDIC-Insured | No |

| Remote Opening | Yes, subject to KYC |

| Xero Integration | Limited; confirm Singapore availability |

4. Revolut Business

Revolut Business is a digital finance platform for companies that need multi-currency accounts, global payments, corporate cards, and software integrations. Revolut Singapore lists business plans from S$0/month and supports 25+ currencies, with Xero, QuickBooks, and NetSuite integrations .

Pros

- Free and paid plans available.

- 25+ currencies supported.

- Strong card, expense, and integration features.

- Xero integration can sync bank feeds, expenses, bills, and invoices .

Cons

- Not a traditional bank account.

- FX allowances vary by plan.

- Extra fees may apply after plan limits or outside market hours.

Best for: Startups with global teams, recurring international payments, and structured expense workflows.

| Revolut Quick Facts | Details |

| Best For | Multi-currency cards and global operations |

| Min. Balance | No public minimum balance |

| Monthly Fee | From S$0/month |

| Currencies | 25+ currencies |

| FX Rate | Interbank allowance; fees after plan limits |

| SDIC-Insured | No |

| Remote Opening | Yes, subject to KYC |

| Xero Integration | Yes |

5. Airwallex Business Account

Airwallex is suitable for companies that collect, hold, convert, and pay in multiple currencies. Its Singapore pricing page states that the free Explore plan supports accounts in 20+ currencies, free local transfers to 120+ countries, Xero and QuickBooks sync, and FX at 0.4% above interbank rates for major currencies and 0.6% for others .

Pros

- Strong multi-currency capability.

- Clear FX margin for common currencies.

- Good for e-commerce, SaaS, agencies, and international trade.

- Xero and QuickBooks integrations.

Cons

- Not a traditional bank.

- Some advanced features require paid plans.

- SWIFT and transaction fees may apply.

Best for: Cross-border startups, e-commerce businesses, import/export companies, and SaaS companies.

| Airwallex Quick Facts | Details |

| Best For | Cross-border payments and multi-currency operations |

| Min. Balance | No public minimum balance |

| Monthly Fee | Free plan available |

| Currencies | 20+ currencies |

| FX Rate | 0.4% above interbank for major currencies; 0.6% for others |

| SDIC-Insured | No; funds safeguarded under local regulations |

| Remote Opening | Yes, subject to KYC |

| Xero Integration | Yes |

Traditional Bank

6. OCBC Business Growth Account

OCBC Business Growth Account is a traditional bank option for Singapore-registered businesses. OCBC states that the account has a S$1,000 initial deposit, S$10 monthly account fee waived for the first two months, and a S$20 fall-below fee if the monthly average balance falls below S$1,000.

Pros

- Established Singapore bank.

- 80 free FAST and 80 free GIRO transactions per month.

- Comes with access to a multi-currency business account with 13 currencies.

- OCBC supports Xero bank feeds through OCBC Velocity .

Cons

- Monthly fee and fall-below fee apply.

- Instant opening is limited to certain Singapore-owned businesses.

- Foreign-owned businesses may need additional review.

Best for: Local SMEs and startups that want a traditional bank with low entry balance and local payment support.

| OCBC Quick Facts | Details |

| Best For | Local SMEs needing traditional banking |

| Min. Balance | S$1,000 |

| Monthly Fee | S$10 monthly fee, waived for the first 2 months; S$20 fall-below fee applies if the monthly average balance falls below S$1,000. |

| Currencies | SGD plus 13-currency multi-currency account |

| FX Rate | Bank FX rates apply |

| SDIC-Insured | Yes, for eligible SGD deposits up to S$100,000 |

| Remote Opening | Yes for eligible local-owned businesses |

| Xero Integration | Yes |

7. CIMB SME Account

CIMB offers traditional business bank accounts with no minimum initial deposit and no monthly fall-below fee for the SME/SME-i account. According to CIMB’s 2026 corporate pricing guide, the SME/SME-i Account has an S$8 monthly account fee, while the TransactPlus/TransactPlus-i Account has an S$28 monthly account fee.

For new-to-bank customers, the monthly account fee may be waived for the first 12 months, subject to CIMB’s terms.

Pros

- No minimum initial deposit for SME/SME-i Account.

- No fall-below fee for SME/SME-i Account.

- Account fee waived for the first 12 months for new-to-bank customers.

- Free FAST, GIRO, payroll payments, and collections via BizChannel for selected accounts.

Cons

- Monthly account fee applies after the waiver period.

- Digital tools may feel less startup-native than fintech providers.

- Foreign-owned or complex structures may require more review.

Best for: Cost-conscious SMEs that want a traditional bank account without a high minimum balance.

| CIMB Quick Facts | Details |

| Best For | SMEs seeking traditional banking with low balance pressure or higher transaction needs |

| Min. Balance | SME/SME-i Account: Nil; TransactPlus/TransactPlus-i Account: check current bank terms |

| Monthly Fee | SME/SME-i Account: S$8/month; TransactPlus/TransactPlus-i Account: S$28/month. Fees may be waived for the first 12 months for new-to-bank customers |

| Currencies | SGD account; foreign currency accounts available separately |

| FX Rate | Bank FX and remittance fees apply |

| SDIC-Insured | Yes, for eligible SGD deposits up to S$100,000 |

| Remote Opening | Online options available, subject to eligibility |

| Xero Integration | Check current bank-feed availability |

8. Maybank FlexiBiz Account

Maybank FlexiBiz Account is positioned as a startup account for Singapore businesses. Maybank lists S$1,000 initial deposit, no monthly fee, and a S$10 minimum balance fee if the average daily balance falls below S$1,000.

Pros

- No monthly account fee.

- Low S$1,000 initial deposit.

- Suitable for basic SGD banking.

- SGD deposits are SDIC-insured up to S$100,000 per depositor per Scheme member.

Cons

- Minimum balance fee applies below S$1,000.

- Online opening is limited to eligible Singapore-incorporated businesses with Singaporean or PR owners/directors.

- Less suited for complex cross-border needs than Airwallex or Wise.

Best for: Local startups that want a simple traditional bank account with a low balance requirement.

| Maybank FlexiBiz Quick Facts | Details |

| Best For | Local startups and simple SGD banking |

| Min. Balance | S$1,000 |

| Monthly Fee | No monthly fee |

| Currencies | SGD; foreign currency accounts available separately |

| FX Rate | Bank FX and remittance fees apply |

| SDIC-Insured | Yes, for eligible SGD deposits up to S$100,000 |

| Remote Opening | Yes for eligible local businesses; others may need branch appointment |

| Xero Integration | Not clearly listed; Financio promotion available |

9. UOB eBusiness Account

UOB eBusiness Account is a traditional SGD business account for startups and SMEs. UOB lists a S$1,000 minimum initial deposit, S$5,000 minimum average daily balance, S$35 annual account fee, and S$15 monthly fall-below fee waived for the account-opening month and the next 11 months.

Pros

- Established Singapore bank.

- 12-month fall-below fee waiver.

- Free FAST, PayNow FAST, and bulk GIRO payroll features are promoted.

- UOB supports Xero bank feeds.

Cons

- S$5,000 average daily balance requirement after waiver.

- Annual account fee applies.

- Mainly SGD-focused unless separate foreign currency products are used.

Best for: Singapore SMEs needing traditional banking, payroll payments, and UOB digital banking tools.

| UOB Quick Facts | Details |

| Best For | SMEs needing SGD banking and payroll payment tools |

| Min. Balance | S$5,000 average daily balance |

| Monthly Fee | S$35 annual account fee; S$15 fall-below fee |

| Currencies | SGD account; foreign currency accounts separate |

| FX Rate | Bank FX and remittance fees apply |

| SDIC-Insured | Yes, for eligible SGD deposits up to S$100,000 |

| Remote Opening | Online application available, subject to eligibility |

| Xero Integration | Yes |

10. DBS Business Multi-Currency Account

DBS Business Multi-Currency Account is a traditional bank account for companies that want SGD plus foreign currency wallets. DBS states that the account supports 13 currencies and offers a Starter Bundle for businesses under three years old, with a S$10 monthly fee and unlimited free FAST and GIRO payments under that bundle.

For standard accounts, DBS states that a S$40 monthly service charge applies unless the average daily balance is at least S$10,000 or equivalent. DBS also notes SDIC protection up to S$100,000 for eligible deposits.

Pros

- Strong traditional bank credibility.

- 13 supported currencies.

- Good for companies planning to scale into financing, trade, and treasury.

- DBS-Xero direct bank feeds are available for DBS business account customers who use Xero.

Cons

- Standard account balance requirements may be high for lean startups.

- Starter Bundle applies only to young businesses.

- Fully online opening is limited to Singapore-incorporated businesses fully owned by Singaporeans or PRs.

Best for: SMEs that need traditional banking, multi-currency wallets, and future access to DBS business finance products.

| DBS Quick Facts | Details |

| Best For | Multi-currency traditional banking |

| Min. Balance | S$10,000 for standard account; Starter Bundle differs |

| Monthly Fee | S$10 Starter Bundle; S$50 annual fee standard account |

| Currencies | 13 currencies |

| FX Rate | Bank FX rates apply; selected SecureFX features available |

| SDIC-Insured | Yes, for eligible SGD deposits up to S$100,000 |

| Remote Opening | Yes for eligible local-owned businesses |

| Xero Integration | Yes |

Traditional banks vs digital business accounts: which is better for startups?

A traditional bank is an established financial institution that offers corporate accounts, loans, trade finance, branch support, and broader banking relationships. Examples include DBS, OCBC, UOB, Maybank, and CIMB.

A digital business account is an online-first financial account used for payments, collections, cards, FX, and expense management. Examples include Aspire, Wise, Airwallex, Revolut, and YouBiz. These providers may be licensed payment institutions or fintech platforms rather than banks.

| Key Factor | Traditional Banks | Digital Business Accounts |

| Advantages | Stronger credibility, loans, branch support, SDIC coverage for eligible SGD deposits | Faster onboarding, lower balance requirements, strong FX and card tools |

| Disadvantages | More paperwork, fall-below fees, stricter onboarding | Usually no SDIC deposit insurance, limited lending, no branch support |

| Best for | Established SMEs, regulated businesses, loan-seeking companies | Startups, foreign founders, online businesses, cross-border teams |

Common mistakes when choosing a startup bank account

Before comparing providers, startups should understand the practical mistakes that often lead to higher costs, slower onboarding, or limited banking support later.

- Focusing only on monthly fees and ignoring FX spreads, SWIFT fees, and fall-below charges.

- Choosing a digital provider when the business needs loans, trade finance, or branch support.

- Choosing a traditional bank when the business mainly needs international payments and fast remote setup.

- Not checking onboarding requirements for foreign directors, foreign shareholders, or holding-company structures.

- Ignoring future needs such as payroll, CPF payments, GST refunds, InvoiceNow, and accounting integration.

What businesses need to know about Singapore banking changes in 2026

Before choosing a business bank account, companies should also understand the key Singapore banking changes in 2026 that may affect payments, invoicing, and compliance.

- Corporate cheques are being phased out. From 1 January 2026, banks will stop issuing new SGD corporate cheque books, and from 1 January 2027, they will stop processing SGD corporate cheques(1) .

- InvoiceNow is becoming more important. IRAS states that businesses applying for voluntary GST registration on or after 1 April 2026 must comply with GST InvoiceNow requirements and transmit invoice data through InvoiceNow-ready solutions(2) .

- CPF e-payments should also be considered. CPF Board states that CPF EZPay allows employers to submit CPF contributions and pay through Direct Debit or PayNow QR(3) .

Why startups and SMEs choose BBCIncorp for company incorporation and banking support

BBCIncorp supports entrepreneurs with Singapore company incorporation, banking preparation, compliance setup, and ongoing corporate administration. For foreign founders, this support can reduce delays because bank onboarding often depends on business activity, ownership structure, source of funds, expected transaction flows, and complete company documents.

BBCIncorp can help with:

- Business incorporation.

- Banking document preparation.

- KYC readiness.

- Company secretary and compliance setup.

- Ongoing corporate support after incorporation.

Need help setting up your Singapore company and preparing for bank onboarding? BBCIncorp can support you from incorporation to banking document preparation, KYC readiness, company secretary setup, and ongoing compliance administration.

For tailored guidance, contact our team at service@bbcincorp.com.

Conclusion

The best business bank account for startups in Singapore is not always the account with the lowest headline fee. A local SME may prefer OCBC, UOB, CIMB, Maybank, or DBS for traditional banking, while a foreign-owned or cross-border startup may find Aspire, Airwallex, Wise, YouBiz, or Revolut more practical.

Before choosing the best business bank account Singapore option, compare onboarding requirements, FX costs, minimum balance rules, accounting integrations, and 2026 digital-payment readiness.

References:

- (1) IRAS – GST InvoiceNow Requirement: https://www.iras.gov.sg/taxes/goods-services-tax-%28gst%29/gst-invoicenow-requirement

- (2) ABS – Guide to E-Payments: https://abs.org.sg/e-payments/guide-to-e-payments

- (3) CPF Board – CPF EZPay: https://www.cpf.gov.sg/employer/making-cpf-contributions/submitting-cpf-contributions-via-cpf-ezpay

Frequently Asked Questions

What is the best business bank account for startups in Singapore?

The best account depends on your operating model. Aspire, Airwallex, Wise, YouBiz, and Revolut may suit startups that need fast onboarding and cross-border payments, while OCBC, DBS, UOB, CIMB, and Maybank may suit businesses that need traditional banking, SDIC coverage for eligible SGD deposits, and future access to loans.

Can foreigners open a business bank account in Singapore?

Yes, foreigners can open a business bank account in Singapore, although approval requirements vary by provider. Banks and digital providers usually review company documents, director and shareholder identities, business activity, source of funds, expected transactions, and KYC risk.

Some traditional banks may require Singpass, local ownership, or in-person verification for certain account-opening flows.

Which business account has the lowest fees?

Among the listed options, Aspire, Airwallex, YouBiz, Wise, and Revolut offer low or no monthly-fee digital account options, while CIMB SME/SME-i Account has no minimum initial deposit and an S$8 monthly fee waived for the first 12 months for new-to-bank customers. The most cost-effective option still depends on FX, transfer volume, and fall-below fees.

What documents are required to open a business account?

Most providers require the company’s UEN, incorporation documents, constitution, business profile, identification documents for directors, shareholders, and authorized signatories, proof of business activity, and information on expected transactions. Foreign-owned companies may need additional documents showing source of funds, ownership structure, and business substance.

How long does business account approval take?

Digital providers may approve straightforward applications within a few business days, while traditional banks can take longer if the ownership structure is foreign-owned, multi-layered, or higher risk. Approval time depends on document completeness, KYC review, business activity, and whether in-person verification is required.

Disclaimer: While BBCIncorp strives to make the information on this website as timely and accurate as possible, the information itself is for reference purposes only. You should not substitute the information provided in this article for competent legal advice. Feel free to contact BBCIncorp’s customer services for advice on your specific cases.

Industry News & Insights

Get helpful tips and info from our newsletter!

Stay in the know and be empowered with our strategic how-tos, resources, and guidelines.