Table of Contents

Cayman economic substance rules require Cayman entities to notify the Tax Information Authority annually. Relevant entities that conduct relevant activities must also satisfy the economic substance test and submit an ES Return within 12 months after their financial year end

In this article, BBCIncorp provides detailed guidance on Cayman Islands Economic Substance, including in-scope entities, compliance procedures, and related considerations.

Key Takeaways

- Cayman economic substance requires in-scope entities to assess whether they are relevant entities, conduct relevant activities, and earn relevant income.

- All Cayman entities should submit an annual Economic Substance Notification, while relevant entities conducting relevant activities must file an Economic Substance Return within 12 months after financial year end.

- The ES test focuses on Cayman-based core income-generating activities, local direction and management, adequate expenditure, premises, and qualified personnel.

- Pure equity holding companies may face a reduced test, while high-risk intellectual property businesses face stricter evidence requirements.

- Non-compliance can trigger financial penalties, information exchange, remedial orders, or strike-off, so records and annual classification should be reviewed carefully.

What is the economic substance in the Cayman Islands?

Cayman economic substance is a compliance framework requiring certain Cayman entities to demonstrate real operational presence in the Cayman Islands when they earn income from defined relevant activities, rather than relying on legal registration alone.

The regime was introduced to align the Cayman Islands with international standards on substantial activities for no-tax or nominal-tax jurisdictions. According to the Department for International Tax Cooperation (DITC), the Economic Substance Act came into force on 1 January 2019 as part of Cayman’s collaboration with the OECD Forum on Harmful Tax Practices and the European Union Commission Services(1).

The current legal basis is the International Tax Co-operation (Economic Substance) Act (2026 Revision), which was published in the Cayman Islands Legislation Gazette on 5 February 2026, consolidated and revised as at 31 December 2025, and replaced the 2024 Revision(2)

For business owners, the key takeaway is simple: a Cayman entity should not only confirm that it exists legally, but also assess whether it is a relevant entity, whether it conducts a relevant activity, whether it earns relevant income, and whether its operations can satisfy the economic substance test.

Importance of economic substance legislation Cayman Islands

Cayman Islands Economic Substance legislation is more than a compliance requirement; it is a strategic framework that reinforces the jurisdiction’s global credibility and commitment to responsible tax practices.

Introduced to align with OECD and EU standards, the regime ensures businesses in Cayman contribute real value to the local economy while maintaining access to international markets and avoiding the reputational risks of being seen as a tax haven.

- Ensures the Cayman Islands complies with international standards, helping avoid EU and OECD blacklists while strengthening investor confidence through genuine local business operations.

- Maintains access to international financial markets by requiring economic substance evidence for cross-border transactions involving Cayman entities.

- Prevents tax avoidance and artificial profit-shifting structures by mandating real economic activities, including personnel, premises, meetings, and operating expenses.

- Enhances regulatory oversight through mandatory Economic Substance Notifications and Returns, enabling the Tax Information Authority (TIA) to monitor compliance and enforce penalties when necessary.

- Encourages sustainable business operations by requiring entities to demonstrate adequate local expenditure, physical presence, and qualified staff in proportion to their income-generating activities.

Who must with Cayman economic substance?

Relevant Entities under Cayman Economic Substance Law

Under Cayman ES Act, in-scope entities, or relevant entities under ES law refer to:

- A company incorporated under the Companies Law (2020 Revision), or

- A Cayman limited liability company (LLC) registered according to the Limited Liability Companies Law (2020 Revision); or

- A limited liability partnership (LLP) registered according to the Limited Liability Partnership Law, 2017; or

- A company incorporated outside of the Cayman Islands and registered under the Companies Law (2020 Revision).

Entities excluded from Economic Substance Law Cayman

There are certain out-of-scope entities, and these cases don’t need to observe the ES test in the Cayman Islands.

Excluded cases are:

- A domestic company;

- A company as an investment fund;

- A company as a tax resident in an overseas jurisdiction

To be regarded as a tax resident in another jurisdiction outside Cayman, your company should provide evidence to the Authority that the company is subject to corporate tax on all of its income in another jurisdiction because of its tax residence, domicile, or other similar reasons.

And this same requirement goes for foreign branches of a relevant entity.

Example

You own a Cayman-incorporated company conducting on a relevant entity from a Hong Kong branch. Since the Hong Kong branch pays corporate taxes on all of the branch’s income in Hong Kong relating to the relevant entity, the branch is regarded as a tax resident outside Cayman.

| IN SCOPE (Relevant Entities) | OUT OF SCOPE (Excluded Entities) |

| Cayman Islands incorporated companies | Domestic companies |

| Limited Liability Companies (LLCs) | Investment funds |

| Limited Liability Partnerships (LLPs) | Entities tax-resident outside the Cayman Islands |

| Foreign companies registered under the Cayman Companies Law | Foreign branches of entities that can demonstrate overseas tax residency |

What are the relevant activities?

The Cayman economic substance law applies when a relevant entity carries on one or more defined relevant activities. These activities are listed in the Act and do not include investment fund business(2) .

The nine relevant activities are: banking business, distribution and service centre business, financing and leasing business, fund management business, headquarters business, holding company business, insurance business, intellectual property business, and shipping business.

| Relevant activity | What to check first |

| Banking business | Whether the entity carries on banking activities under the applicable Cayman banking framework. |

| Insurance business | Whether the entity accepts insurance risk, reinsures risk, or carries on regulated insurance activity. |

| Fund management business | Whether the entity manages securities for an investment fund under the applicable licensing or authorization framework. |

| Financing and leasing business | Whether the entity provides credit facilities for consideration, excluding activities carved out by the Act. |

| Headquarters business | Whether the entity provides senior management, risk control, or substantive risk-related advice to group entities. |

| Distribution and service centre business | Whether the entity buys goods from group entities for resale outside Cayman, or provides services to group entities outside Cayman. |

| Shipping business | Whether the entity operates ships for international transport or related shipping activities. |

| Holding company business | Whether the entity is a pure equity holding company that only holds equity participations and earns only dividends and capital gains. |

| Intellectual property business | Whether the entity holds, exploits, or receives income from intellectual property assets. |

A Cayman entity should not assume that a passive or simple structure is automatically out of scope. For example, a pure equity holding company may be subject to a reduced ES test, while high-risk intellectual property business is subject to a stricter presumption and evidential burden.

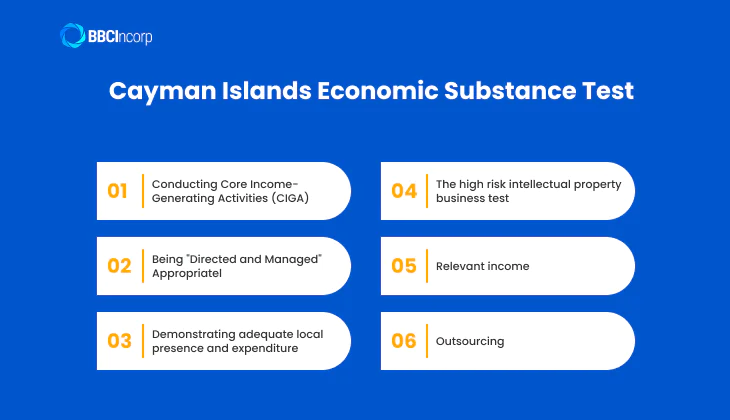

What is the economic substance test in the Cayman Islands?

The Cayman Islands Economic Substance Test (ES Test) requires entities engaged in certain geographically mobile activities to demonstrate that they maintain a genuine operational presence within the jurisdiction.

Introduced in line with OECD international standards, the regime aims to prevent the artificial shifting of profits to low- or no-tax jurisdictions.

| Requirement | Summary |

| CIGA | Core income-generating activities must be carried out in the Cayman Islands and be relevant to the entity’s business activity. |

| Directed and Managed | Strategic decisions and board oversight must take place in the Cayman Islands, with proper records maintained locally. |

| Adequate Presence | The entity must have adequate local expenditure, physical presence, and qualified personnel in Cayman. |

| High-Risk IP Business | High-risk IP entities face stricter substance requirements and must provide additional evidence of compliance. |

| Relevant Income | Substance requirements are assessed based on income generated from Relevant Activities. |

| Outsourcing | CIGA may be outsourced within Cayman if the entity retains control and oversight of the activities. |

Conducting Core Income-Generating Activities (CIGA) in Cayman

Core income-generating activities (CIGA) are activities that are central to generating income from a Relevant Activity. These activities must be carried out in the Cayman Islands and may differ depending on the specific type of business the entity engages in.

For example, in a finance and leasing business, CIGA might include negotiating funding terms, setting lease terms, and managing credit risks. For intellectual property businesses, CIGA could involve research and development or managing legal protections for the IP.

The ES Act recognizes that not every entity will perform all CIGA listed for a particular Relevant Activity. However, the activities that an entity does undertake must be performed locally. The Cayman Islands authorities do not require a rigid checklist but instead adopt a “principles-based approach” that considers the nature and scale of each entity’s business.

Entities may outsource CIGA to service providers located in Cayman, but they must retain control and oversight. The outsourcing arrangement must be verifiable, and the service provider must register with the Department for International Tax Cooperation to confirm the authenticity and scope of the services provided.

Being “Directed and Managed” appropriately

An entity must also be directed and managed in an appropriate manner in relation to the Relevant Activity, and this direction and management must occur in the Cayman Islands. This requirement is focused on ensuring that strategic decision-making is not simply rubber-stamped offshore but is genuinely executed within Cayman.

Key elements to consider include:

- The board of directors should collectively possess sufficient expertise relevant to the activity being conducted.

- Meetings of the board must be held in the Cayman Islands with adequate frequency and a quorum of directors physically present.

- Strategic decisions must be clearly documented in meeting minutes, which should also be kept in the Cayman Islands.

- Other appropriate records and corporate documents should be maintained locally.

Even for entities with minimal activity, the expectation is that at least one board meeting is held in Cayman annually. This component of the economic substance test Cayman emphasizes the importance of having genuine oversight and strategic control based in the jurisdiction.

Demonstrating adequate local presence and expenditure

The third pillar of the ES Test requires an entity to demonstrate an adequate level of economic presence in the Cayman Islands, commensurate with the relevant income it generates. This includes three key factors:

- Operating Expenditure: Entities must incur adequate operating costs in or from within the Cayman Islands. This includes expenses such as rent, utilities, payroll, and service fees that are proportionate to the scale of the business.

- Physical Presence: Entities should have a tangible physical presence in Cayman. This can include a registered office, owned or leased premises, or equipment relevant to the business operations. Mere registered office or mail-forwarding arrangements are generally insufficient for entities that must demonstrate a substantive physical presence under the ES Test.

- Qualified Personnel: The entity must employ or contract with a sufficient number of qualified individuals located in the Cayman Islands. These employees should have the skills and experience necessary to carry out the core income-generating activities of the business.

Importantly, there is no fixed formula for determining what is “adequate” or “appropriate.” The determination depends on the size, complexity, and nature of the business. Relevant Entities are expected to keep records that justify their internal assessment of adequacy, in good faith, based on their operations and income levels.

The high risk intellectual property business test

Entities engaged in “high risk intellectual property business” face a heightened burden under the ES Test. A business is classified as high risk if, for instance, it holds IP that it did not create, and derives income from licensing it to affiliated group entities or as a result of the work of other group entities.

Such entities are presumed not to meet the ES Test unless they can provide compelling evidence to the contrary. This includes:

- Demonstrating that control over the development, exploitation, and maintenance of the IP is exercised in Cayman.

- Employing a sufficient number of full-time, qualified staff who permanently reside in Cayman or conduct their activities there.

- Providing comprehensive documentation of the entity’s IP management and operations.

The DITC will only consider the presumption rebutted if all required evidential thresholds are met, reflecting the significant scrutiny applied to IP-heavy business models under the Cayman regime.

Relevant income

“Relevant income” refers to all gross income derived by a Relevant Entity from its Relevant Activities, recorded according to applicable accounting standards. The amount of relevant income is used to determine what constitutes “adequate” operating expenditure, physical presence, and personnel.

If a Relevant Entity is conducting a Relevant Activity but has no relevant income during a given financial year, it is not required to satisfy the ES Test for that period. However, it must still meet notification and reporting obligations by submitting a “nil return” to the DITC. This ensures transparency even when income is not being generated.

Outsourcing

Outsourcing can be a legitimate way for entities to satisfy certain elements of the ES Test, particularly the conduct of CIGAs. However, outsourcing is only acceptable if:

- The service provider is located in the Cayman Islands.

- The Relevant Entity can demonstrate effective control and monitoring over the outsourced activities.

- The service provider is registered with the DITC and can independently verify the engagement and the nature of the services provided.

Outsourcing to service providers outside the Cayman Islands is not permitted for purposes of meeting the ES Test. Additionally, any domestic outsourcing must be backed by timely verification from the provider—within 30 days of reporting to the DITC—to ensure credibility and prevent abuse.

Outsourcing does not absolve the Relevant Entity of its responsibilities. Ultimate accountability for meeting the ES Test remains with the entity itself, even if operations are delegated to a local partner.

Filing requirements under Cayman ES (What to report)

All entities must file an annual Economic Substance Notification (ESN) via the General Registry. Additionally, relevant entities conducting relevant activities must submit an Economic Substance Return (ESR) to the Tax Information Authority within 12 months after their financial year-end.

| Feature | Economic Substance Notification (ESN) | Economic Substance Return (ESR) |

| Who must file? | All registered Cayman entities | Relevant Entities conducting Relevant Activities |

| Filing Authority | General Registry (CAP Portal) | Tax Information Authority (TIA) via DITC Portal |

| Deadline | Annually before 31 January (or before filing the annual return through CAP)(3) | Within 12 months after the end of the financial year(4) |

| Purpose | Declares the entity’s Economic Substance status and Relevant Activities | Demonstrates compliance with the Economic Substance Test |

| Penalty for Late / Non-Filing | Administrative consequences may apply and annual return processing may be affected | CI$5,000 base + CI$500/day for late filing(5) |

Economic Substance Notification (ESN)

What is an Economic Substance Notification?

An Economic Substance Notification (ESN) is an annual filing requirement under the Cayman Islands Economic Substance regime. It serves as a preliminary disclosure through which entities report whether they are carrying on a Relevant Activity and whether they qualify as a Relevant Entity under the Economic Substance Act.

The information provided in the ESN helps determine whether the entity is required to submit a full Economic Substance Return (ESR) to the Tax Information Authority (TIA).

How to file an Economic Substance Notification

Economic Substance Notifications are submitted electronically through the Corporate Administration Platform (CAP) operated by the Cayman Islands General Registry.

The ESN is typically completed as part of the entity’s annual return process and must be filed before the annual return can be finalized.

What information is included in an ESN?

Depending on the entity’s circumstances, an ESN may require information such as:

- Whether the entity is carrying on one or more Relevant Activities;

- Whether the entity qualifies as a Relevant Entity;

- The entity’s financial year-end date;

- Whether the entity claims tax residency in another jurisdiction;

- Details and supporting evidence relating to overseas tax residency claims (where applicable);

- Information relating to parent entities, ownership structures, or ultimate beneficial owners where required by the Authority.

When to file an ESN

The ESN must be completed annually through the CAP system as part of the entity’s annual return obligations with the General Registry.

Economic Substance Return (ESR)

What is an Economic Substance Return?

An Economic Substance Return (ESR) is an annual filing required from Relevant Entities that carry on Relevant Activities and generate Relevant Income during a financial year.

The purpose of the ESR is to enable the Tax Information Authority (TIA) to assess whether the entity has satisfied the Economic Substance Test under Cayman Islands law.

How to file an Economic Substance Return

The ESR is submitted electronically through the DITC Portal, which is administered by the Department for International Tax Cooperation (DITC).

The entity’s designated Responsible Person will receive access to the portal and may authorize additional users to assist with preparing and submitting the return.

What information must be included in an ESR?

Entities may be required to provide:

- The Relevant Activity or Relevant Activities conducted;

- The amount and type of Relevant Income earned;

- Operating expenditure attributable to the Relevant Activity;

- Details of assets, premises, equipment, or facilities used in the Cayman Islands;

- Information on qualified employees and personnel involved in the activity;

- A description of the Core Income-Generating Activities (CIGA) performed;

- Details of any outsourced activities conducted in the Cayman Islands;

- Information relating to multinational enterprise (MNE) group membership, where applicable;

- Additional information for intellectual property businesses, including high-risk intellectual property businesses;

- Any supporting documentation requested by the TIA.

When to file an ESR

Relevant Entities must submit their ESR within 12 months after the end of their financial year.

Example

| Financial Year End | ESR Filing Deadline |

| 31 December 2025 | 31 December 2026 |

| 30 June 2025 | 30 June 2026 |

Tax Resident Outside Cayman Islands (TRO) Filing

Where an entity conducts a Relevant Activity but claims to be tax resident in another jurisdiction, it must provide evidence supporting that claim through the DITC Portal.

Supporting documentation typically includes:

- A valid tax residency certificate; or

- Other official evidence demonstrating that the entity is subject to tax in another jurisdiction due to residence, domicile, or a similar connecting factor.

The relevant filing and supporting documentation must generally be submitted within 12 months after the end of the entity’s financial year.

Record keeping and exchange of information

Under the ES Law (2020 Revision), the Authority shall share information collected by the Authority under the Economic Substance Law with other competent authorities as per signed agreements and associated global standards.

Accordingly, the entity will need to conduct the information exchange if the entity falls into the following cases:

- The relevant entity failed to fulfill the ES test regarding its relevant activities;

- The relevant entity relates to a high-risk IP business.

Be advised that information will also be shared between the Authority and the relevant authority of the jurisdiction in which the entity in question is proven to be a tax resident, and where the parent company, ultimate parent company, and ultimate beneficial owner of the relevant entity resides (as the case may be).

In the Cayman Islands, entities conducting relevant activities must maintain records demonstrating compliance with the Economic Substance Test. These records must be kept for six years following the end of the relevant financial year and should include information provided in the Economic Substance Returns. Failure to maintain proper records can result in penalties.

How should a Cayman entity prepare for ES compliance?

A Cayman entity should start with classification, then confirm filing obligations, gather operating evidence, and review whether its Cayman substance matches the relevant activity and income.

Use the following process before each annual filing cycle:

- Confirm the entity type:Identify whether the entity is a company, limited liability company, partnership, limited liability partnership, foreign company, investment fund, or another structure covered by the Act.

- Check relevant activities: Review the entity’s income streams, contracts, group transactions, assets, and management functions to determine whether any of the nine relevant activities apply.

- Confirm relevant entity status: Check whether the entity is excluded as an investment fund, domestic company, or entity tax resident outside the Cayman Islands.

- Assess relevant income: Identify gross income from each relevant activity, using the applicable accounting records.

- Map CIGA and decision-making: Record which CIGA are performed, where they are performed, who performs them, and how board oversight is documented.

- Check adequacy of Cayman substance: Review local expenditure, premises, personnel, service provider arrangements, meeting minutes, and supporting records.

- Prepare ESN, ES Return, or TRO documentation: File through the appropriate Cayman portal and retain proof of submission.

- Keep records for six years: The Act requires a relevant entity subject to the ES test to retain relevant books, documents, records, and electronic information for six years after the end of the financial year.

Penalties for Non-compliance cases of Cayman Islands Economic Substance

Failing to meet Cayman economic substance requirements carries escalating financial penalties — and in persistent cases, entity strike-off and automatic information-sharing with the entity’s home-country tax authority. The penalty structure is designed to be progressive, with significantly higher fines for repeated non-compliance.

| Violation | Penalty (CI$) | Approx. USD |

| Late or non-filing of ESR | CI$5,000 + CI$500/day(6) | ~USD 6,100 base, accruing daily |

| Late or non-filing of ESN (after 31 March) | CI$500/day | ~USD 610/day, accruing daily |

| Failing the ES Test — first financial year | CI$10,000 | ~USD 12,200 |

| Failing the ES Test — second consecutive year | CI$100,000 | ~USD 121,950 |

| Persistent non-compliance (two consecutive failures) | Grand Court application — entity struck off or ordered to take remedial action | Entity dissolved |

| Information sharing trigger | DITC automatically shares information with the home-country tax authority of any entity that fails the ES Test | Potential tax and reputational exposure in home jurisdiction |

| Knowingly supplying false information to TIA | CI$10,000 fine and/or 5 years imprisonment on summary conviction | ~USD 12,200 |

Important notice

Additionally, under international transparency agreements, the TIA is legally obligated to spontaneously exchange information regarding non-compliant entities with the tax authorities of the jurisdiction where the parent company, ultimate parent company, or ultimate beneficial owner is a tax resident.

BBCIncorp supports your Economic Substance Compliance in the Cayman Islands

At BBCIncorp, we assist businesses in navigating the complexities of Economic Substance compliance in the Cayman Islands. With a deep understanding of local regulations and international tax standards, we offer reliable support so your business remains fully compliant while focusing on growth.

Our team assists Relevant Entities in assessing whether their activities fall under the scope of the Economic Substance Act, and if so, guides them through the preparation and submission of Economic Substance Returns. We also help clients maintain the proper documentation required to demonstrate core income-generating activities, local management, and adequate presence within the jurisdiction.

In addition to compliance, BBCIncorp offers a full suite of offshore business services. If you are looking to verify your company’s good standing status, visit our guide to the Cayman Islands Certificate of Good Standing. For those interested in incorporation or learning about the Cayman Islands company registry, we provide detailed resources and ongoing support.

Conclusion

Cayman economic substance compliance starts with proper classification. A Cayman entity should determine whether it conducts a relevant activity, whether it is a relevant entity, whether it earns relevant income, and whether it can evidence the ES test through local activity, governance, expenditure, presence, personnel, and records.

For support with Cayman company setup, statutory maintenance, and ES compliance review, contact BBCIncorp or explore our Cayman Islands company formation service.

References:

- (1) Economic Substance: https://www.ditc.ky/es/

- (2), (3), (4), (5), (6) INTERNATIONAL TAX CO-OPERATION: (ECONOMIC SUBSTANCE) ACT (2026 Revision) Supplement No. 10 published with Legislation Gazette No. 7 dated 5th February, 2026

- (7) Tax Information Authority: https://www.ditc.ky/wp-content/uploads/Economic-Substance-Guidance.pdf

Frequently Asked Questions

What is the difference between an ESN and an ESR?

An Economic Substance Notification (ESN) and an Economic Substance Return (ESR) are distinct but related filings required under the economic substance regulations.

The ESN is a preliminary notification that confirms whether an entity is conducting “relevant activities” and collects basic information. The ESR, on the other hand, is a more detailed report that demonstrates how the entity satisfies the Economic Substance Test for those relevant activities.

What happens if my company fails the Economic Substance Test?

If your company fails the Economic Substance Test in the Cayman Islands, it may face serious financial and legal consequences. An initial failure can result in a penalty of up to US$12,195. If the failure continues in a subsequent year, the fine may rise to US$121,950, and the Registrar must apply to the Grand Court for further action, including possible strike-off.

Failure to file required reports may incur additional fines, starting at US$6,098 with daily penalties of US$610. Companies that misclassify themselves or ignore requests from the DITC risk maximum penalties or even imprisonment for non-compliance.

What are the specific CIGA for my business activity?

To determine the specific Core Income-Generating Activities (CIGA) for your business, you must identify the key functions that contribute to your company’s revenue and ensure they are carried out within the relevant jurisdiction. The exact CIGA depends on your business activity.

For example, a financing and leasing business would include activities such as negotiating funding terms, acquiring assets, setting lease conditions, and managing financial risks. A shipping business might involve managing the crew, maintaining vessels, overseeing deliveries, and organizing voyages.

When is the ES Return due in the Cayman Islands?

The ES Return is due within 12 months after the last day of the relevant entity’s financial year. For example, if the financial year ends on 31 December, the ES Return is generally due by 31 December of the following year.

What if a relevant entity has no relevant income?

If a relevant entity conducts a relevant activity but earns no relevant income in the financial year, it should still review its ESN and reporting position carefully. The ES test is assessed by reference to relevant income, but classification and reporting obligations may still apply depending on the entity’s facts and DITC requirements.

Are investment funds subject to Cayman economic substance requirements?

Investment funds are excluded from the definition of relevant entity under the Act. However, the exclusion should be reviewed carefully because an entity through which a fund invests or operates may still need separate analysis, especially if it is not itself the ultimate investment held by the fund.

What evidence is needed for a tax resident outside Cayman claim?

The Cayman Islands Guidance states that satisfactory evidence may include tax residence certificates or letters, tax assessments, tax demands, proof of tax payment, tax returns, or rulings from the competent tax authority of the other jurisdiction. Without satisfactory evidence, the entity may be treated as a relevant entity subject to the ES Act(7)

Disclaimer: While BBCIncorp strives to make the information on this website as timely and accurate as possible, the information itself is for reference purposes only. You should not substitute the information provided in this article for competent legal advice. Feel free to contact BBCIncorp’s customer services for advice on your specific cases.

Industry News & Insights

Get helpful tips and info from our newsletter!

Stay in the know and be empowered with our strategic how-tos, resources, and guidelines.